-

Moody’s recent credit downgrades for the US, along with data on housing and retail revenues, are set to capture attention this week.

-

Snowflake appears to be a solid buy, boasting strong revenue and positive guidance ahead.

-

Target, on the other hand, is experiencing a decline in revenue and profits, making it a candidate for selling off.

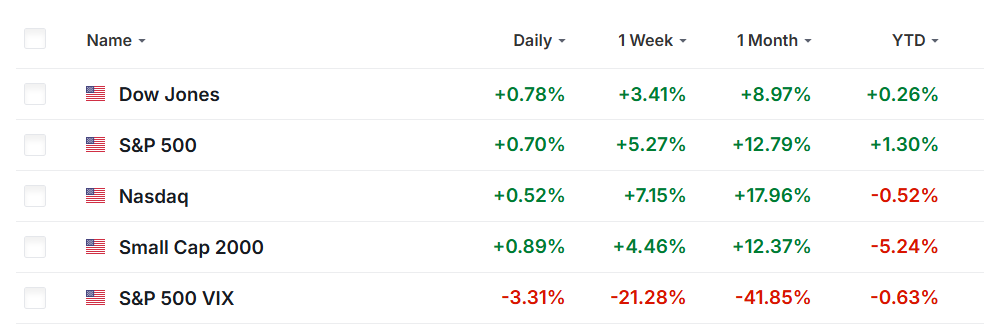

Stock markets wrapped up higher on Friday, reflecting positive gains over the week, driven by confidence around the trade situation and newfound optimism regarding AI investments.

This past week saw the Dow Jones industrial average climb 3.4%, while the S&P 500 rose by approximately 5.3%. The tech-heavy NASDAQ composite surged by 7.2%, allowing the Dow and S&P to recoup earlier losses from the year.

In line with these developments, investors may face increased volatility as they continue to evaluate economic conditions, inflation, interest rates, and corporate earnings. Notably, Moody’s downgraded the US credit rating from “AAA” to “AA1,” a move attributed to rising debt and interest obligations.

This week’s economic calendar is drawing attention, particularly the Flash PMI readings for manufacturing and services and updates on the housing sector.

According to futures markets, traders believe there’s at least a 90% likelihood that the Federal Reserve will hold steady during its June meeting.

Additionally, results from major retailers, including Home Depot, Lowe’s, Target, and TJX, will be critical as the reporting season remains relatively quiet. Other notable reports expected include Palo Alto Networks, Snowflake, Intuit, and Baidu.

Regardless of market movements, there’s focus on stocks that may see increased demand, as well as those exhibiting signs of weakness. It’s important to note that my focus is just for this week, from Monday to Friday.

Snowflake, a player in data analytics and cloud software, is anticipated to deliver its first-quarter revenue report on Wednesday, which could serve as a positive catalyst.

Analysts are increasingly bullish, with profit estimates being raised 19 times in recent weeks, compared to just 10 reductions. This upward trend indicates growing confidence in Snowflake’s short-term performance.

For the quarter ending in April, analysts expect adjusted earnings to increase by $0.21 per share, marking a significant 51% year-over-year growth, while revenues are forecasted to rise by 22%, exceeding $1 billion. Such figures reflect Snowflake’s resilience in broadening its enterprise customer base amid concerns surrounding tech spending.

Once strictly a data analytics company, Snowflake has evolved into a comprehensive cloud data platform, tapping into trends in AI and big data analytics. Its AI toolkit has found notable traction and allows businesses to harness predictive analytics. Moreover, there’s recognition of improved adoption of SnowPark, which broadens its developer applications beyond basic analytics.

Given these factors, Snowflake’s management is poised to provide strong sales guidance this quarter and onwards, benefiting from a substantial rise in AI adoption, customer retention, and strategic growth initiatives.

Market experts are forecasting a potential revenue swing in Snowflake’s stock due to options market movements, which indicate a possible fluctuation of about 10.8% in either direction. Following a rally that began from a low of $120.10 in April, the stock closed Friday at $183.08, showing a robust performance.

Despite some concerns around its credit rating, Snowflake’s technical outlook remains strong, indicating a “buy” signal across both short and long-term time frames.

Meanwhile, Target’s situation is notably more challenging as it gears up for its first-quarter results. Traders are understandably cautious, factoring a possible 10.4% price swing for Target’s stocks following the earnings report.

The sentiment among analysts has deteriorated, with all 22 keeping tabs on Target reducing their profit estimates leading up to the report.

Wall Street is predicting earnings of $1.69 per share for Target, down nearly 19% year-over-year, with revenues estimated to dip about 1% to $24.4 billion. These projections starkly reveal the struggles Target faces in maintaining sales momentum and profitability in today’s retail climate.

Big-box retailers are grappling with numerous challenges, such as reduced store traffic and softer spending on discretionary items, compounded by potential pressures from tariffs affecting supply chains.

Additionally, there’s concern over customer reactions to the company’s diversity and inclusion initiatives, with some analysts suggesting boycotts might be hindering store visits.

I think it’s likely that CEO Brian Cornell will exercise caution in providing guidance for the year ahead, given the tough operating conditions and competitive landscape.

Recently, Target shares dropped below $100 for the first time since April 2020, closing at $98.58. The common moving averages reflect a steep decline of over 27% thus far in 2023, underperforming the broader market.

It’s worth mentioning that Target currently holds a financial health score of 2.5 out of 5, highlighting ongoing worries surrounding profitability and inconsistent sales growth.

The opinions in this piece are entirely those of the authors and should not be construed as investment advice.