Are you currently receiving Social Security retirement benefits? If so, you may want to mark October 10th on your calendar. Then you'll know how big your monthly payments will be in 2025. Hopefully that's enough of an improvement to offset the price increases for pretty much everything so far this year.

But how much of an increase is required? For that matter, what does it mean in practical terms for the program's current beneficiaries?Keep reading.

Cola is here!

What the heck is cola? Abbreviation for “cost of living adjustment.” Recognizing that the cost of living increases over time, the Social Security Administration periodically increases payments to beneficiaries in all programs. Of course, the most-watched COLA update is the one that affects 67.7 million people, including roughly 53.2 million people age 65 and older.

of social security The government has not provided any official hints about what the COLA will be in any given year. But we have a rough idea of what's going to happen. Data from the Bureau of Labor Statistics shows overall costs for consumers have increased by 2.5% since the entitlement program last issued COLAs in October 2023. Excluding volatile food and fuel prices from the calculation, consumer prices will rise by 3.2% in October 2023. Same 12 month stretch. The latest estimates from the Federation of Senior Citizens show an increase of 2.5%.

In other words, it would be surprising if there wasn't an increase, at least within that range.

What this means in simpler terms is that the average monthly Social Security payment this year is $1,907, so a 2.63% increase would mean the average monthly benefit in 2025 would be about $1,957. That's $50 more per month. However, note that those receiving larger payments will see a larger nominal increase, while retirees who are currently cashing smaller-than-average checks will see a smaller net improvement. Everyone sees the same COLA, but it's a percentage-based improvement compared to your current monthly benefit.

Can overcome lackluster cost of living adjustments

But no matter how much money you have, isn't it enough? If you feel this way, you're not alone.

Social Security COLAs are based on official inflation data from the U.S. Bureau of Labor Statistics; rear Fundamental price increases are being implemented and the economy is already suffering. By the time you see any benefits, you may have recouped your bill.

It's also arguable that annual COLAs don't reflect reality, especially for retirees, who are likely to spend more on health care than the average worker. That's what the Seniors Alliance's crunch of numbers shows, anyway. This study suggests that over the past 15 years, the average U.S. retiree receiving Social Security benefits actually lost $370.23 worth of monthly purchasing power that they theoretically shouldn't have lost. .

While there's not much that can be done about Social Security's future cost-of-living adjustments, there are a few things retirees can do to make up for inadequate COLAs. Here are three that may be most helpful.

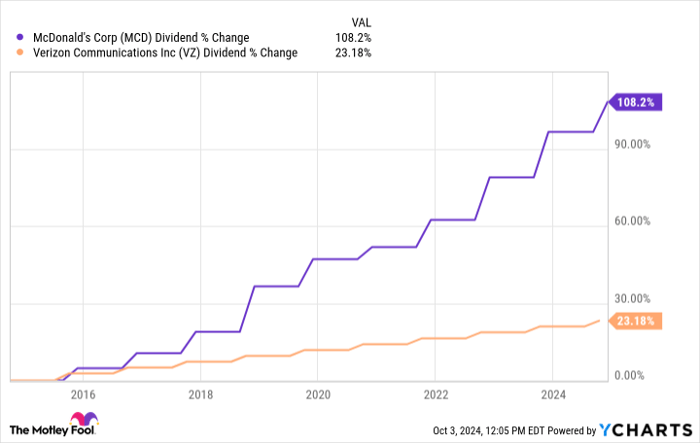

1. Review dividend stocks

If you own any stocks, you probably own at least some dividend-paying stocks. But are your dividend stocks the best? dividend stocks In your portfolio? If overall dividend growth doesn't reliably outpace inflation, it might not. for example, verizonThe telecom giant's forward dividend yield of 6% is impressive, since the telecom giant's dividend has increased at an average rate of only about 2% per year since 2014. vice versa, mcdonalds The current yield is 2.33%, but the quarterly dividend has more than doubled over the past 10 years.

MCD dividend Depends on the data Y chart.

Importantly, if you rely on dividend stocks to generate spendable income, you may actually be losing purchasing power over time without realizing it.

2. Reconsider your bond holdings

I want to review dividend stocks, so it might not be a bad idea to review them. bond, CDand other fixed income products either… Especially now, as interest rates continue to fall from multi-year peaks.

Just like stocks, your bond portfolio should always be diversified. It may be worth locking in your holdings a little longer at higher-than-usual interest rates before the Fed implements its plan to lower interest rates over the next few years.

3. Not all “cash” is the same

Given that you may currently hold at least some of your savings in cash, consider moving some of that money into a high-yield money market fund. These funds are Just under 5% And that yield is likely to fall in line with overall interest rates. But that's a huge amount considering you're earning virtually nothing with the cash you have in your checking and savings accounts.

There seems to be a pitfall… While the funds in most checking accounts are always readily available, and savings accounts often have next-day access, cashing out most of the assets you hold in the money market immediately after purchase can save you a small amount of money. Early redemption fees may apply. You should check with your bank or broker for details about the money market you have in mind. Fortunately, the expected minimum holding period is usually only a few weeks, and if you really need this cash during that time, can Get to it.

Image source: Getty Images.

There's a fourth, less desirable option…but it may not be as dire as you fear. In other words, back to work.

You probably weren't thinking about going back to work at this point in your life. But living with the stress of not having enough income to spend is probably not what you had planned either. You need to find a balance.

Don't worry. Once you start receiving Social Security retirement benefits, working until your income reaches a certain threshold will not affect your payments. For reference, beneficiaries can earn up to $22,320 this year before the Social Security Administration begins reducing the amount of their monthly checks. You don't even need to earn that much if your only goal is to cope with the rising cost of living.

Please keep your eyes and ears open for the 10th. When that happens, the big questions about COLA will be answered.

$22,924 Social Security Bonuses Most Retirees Completely Overlook

If you're like most Americans, you're several years (or more) behind on your retirement savings. But some little-known “Social Security secrets” can help ensure a boost to your retirement income. Example: One simple trick can pay you as much as $.22,924 Plus…every year! By learning how to make the most of your Social Security benefits, we think you can retire confidently with the peace of mind we all desire. Click here to learn more about these strategies.

View “Social Security Secrets” »

james bramley has no position in any of the stocks mentioned. The Motley Fool recommends Verizon Communications. The Motley Fool has Disclosure policy.