Reflections on the Dot-Com Bubble and Current Market Trends

The dot-com bubble, which famously burst 25 years ago, still influences today’s market, especially as we ride a current bull phase driven by technological advancements. The rising interest in artificial intelligence, particularly since OpenAI introduced ChatGPT three years ago, has significantly contributed to market performance.

Over the past three years, we’ve seen impressive market gains. For instance, the Nasdaq index, heavy on tech stocks, has increased by 104%. Notably, Nvidia, a leader in AI semiconductor technology, has become the most valuable company on Wall Street, boasting a market cap of $4.4 trillion.

Yet, the rapid ascent of these stocks raises alarms about the possibility of a new tech bubble. Skeptics suggest a downturn is inevitable.

However, not everyone shares that concern. For example, Larry Adam, the Chief Investment Officer at Raymond James, argues that comparing the current situation to the dot-com era is exaggerated. He feels the present upswing isn’t as precarious.

Adam noted, “Though discussions of an AI bubble pervade the media, we believe the long-term perspective on technology remains optimistic. The normal fluctuations associated with innovation cycles won’t likely derail our positive outlook on stocks. Given the enduring impact and transformative nature of the AI boom, we’re still supportive of the tech sector, especially with industries fueling data center growth.”

Raymond James analysts are recommending that investors consider two tech stocks with strong ties to AI and cloud computing. In fact, we took a deeper dive into these recommendations to understand their potential better.

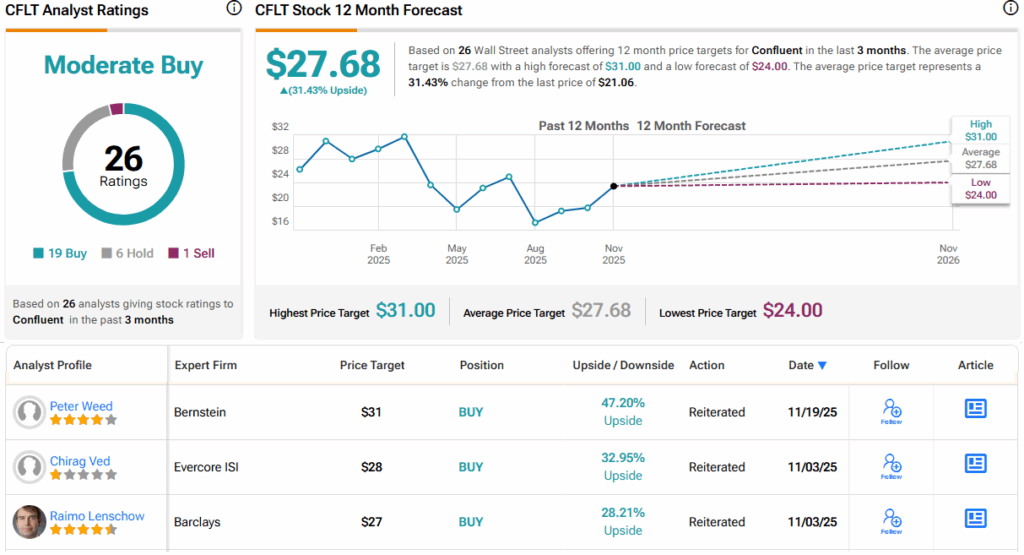

Confluent Co., Ltd. (CFLT)

First up, Confluent. This tech company was founded in 2014 and has developed a comprehensive data streaming platform built on the renowned capabilities of Apache Kafka and Apache Flink. Their platform aims to simplify the often overwhelming nature of raw data, comparing it to a bowl of spaghetti—quite daunting at first glance, but manageable with the right approach.

Through its platform, Confluent transforms data into valuable streams that serve various purposes, such as real-time inventory management for retailers, fraud detection for banks, and diagnostics for assembly lines in manufacturing. What unites these sectors is the urgent need to swiftly and accurately turn large data volumes into practical insights.

Confluent has made a name for itself in data streaming, rising to become a $7.3 billion player in this field. A significant 70% of Fortune 500 companies count on their services for essential operations. The platform also reportedly reduces data management costs by 25% and yields a fivefold return on investment through quicker data access and responsiveness.

As of September 30 this year, they reported 2,533 customers with a recurring annual revenue exceeding $20,000. Among these, 1,487 have an ARR of $100,000 or more, reflecting a 10% increase year-on-year.

In Q3 2025, Confluent achieved $298.5 million in revenue, marking a 19% increase from the previous year and surpassing expectations by $5.63 million. The adjusted earnings per share stood at $0.13, also exceeding analyst predictions.

Mark Cash, a Raymond James analyst, perceives the company as well-positioned for ongoing success. He stated, “As pressures for optimization ease and new applications emerge, the consumption of cloud products has accelerated within our core Streaming and DSP offerings. Our outlook remains optimistic about Confluent’s capacity to leverage its Streaming capabilities for lasting growth.” Cash mentioned that RPO surged by 43% year-over-year, indicating Confluent’s growing significance in a landscape marked by forecasting hurdles.

Cash rates CFLT as an Outperform (or Buy), with a price target of $30, suggesting a potential upside of 42% over the coming year. Recent reviews from analysts show a consensus that leans towards a Medium Buy, with the current stock at $21.06 and an average target of $27.68, indicating a possible one-year upside of 31%.

Lattice Semiconductor (LSCC)

Next on the list is Lattice Semiconductor, a smaller player in the chip market, with a market cap of $9.4 billion and last year’s sales hitting $509.4 million. While not in the same ballpark as Nvidia, Lattice remains consistently profitable, carving out a vital niche in the industry.

Lattice focuses on the design and production of low-power field programmable gate arrays (FPGAs) that are crucial in semiconductor technology. These chips can be easily programmed and repurposed, making them highly adaptable to fluctuating technology needs. Their applications span across AI, edge computing, factory automation, 5G, and cybersecurity, among others.

The company offers a range of FPGA products, from general-purpose to specialized chips for video connectivity, and backs them with various tools, including software and training resources.

For Q3, Lattice reported revenue of $133.35 million—a 5% increase from the previous year and 7.6% from the prior quarter. This figure exceeded expectations by $341,000.

Ultimately, they shared a non-GAAP EPS of 28 cents, a 4-cent increase compared to the same period last year, meeting analyst forecasts.

Analyst Srini Pajuri from Raymond James sees solid potential here, noting the company’s successes and bright future. He remarked, “LSCC continues to gain from upgrades in public cloud infrastructure, with increased FPGA usage in both general and AI server setups.” Pajuri also mentioned a decline in contributions from the industrial and automotive sectors, which persists but is expected to normalize by year-end, aligning with broader patterns in the market.

Pajuri rates LSCC as an Outperform (Buy) with a target price of $80, suggesting a potential 17% increase within a year. The stock currently trades at $68.47, with Wall Street analysts giving it a Moderate Buy consensus rating based on 11 reviews—9 Buys, 1 Hold, and 1 Sell. The average price target stands at $79.40, hinting at a 16% upside in the next 12 months.