Millions of student loan borrowers can now relax a bit as the Department of Education has decided to restart several significant loan forgiveness programs.

This week, the White House announced that loan forgiveness will resume for qualified borrowers under two different income-driven repayment plans that had previously been on hold.

“Honestly, this is a major development,” noted consumer finance expert Erica Sandberg. “Millions of borrowers will find relief.”

Why was student loan forgiveness paused?

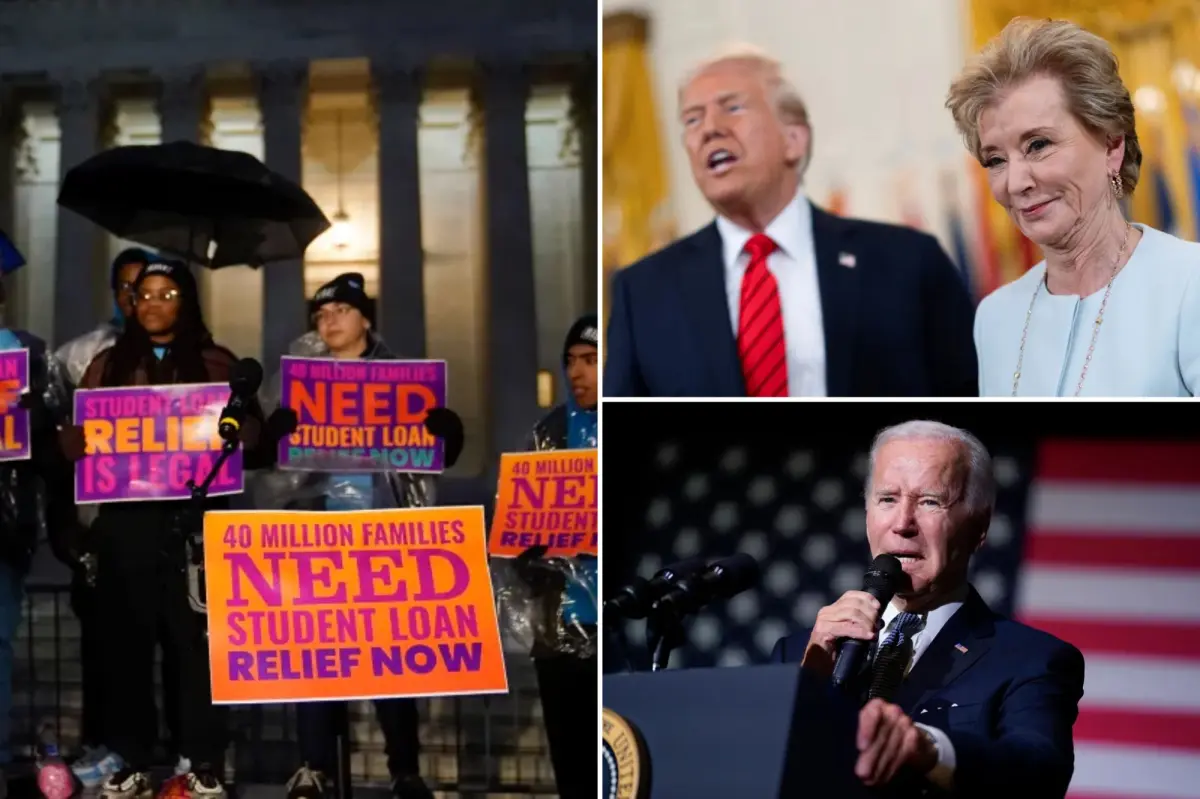

Back in February, an appeals court upheld a decision that halted a repayment program initiated during the Biden administration, known as SAVE, which had offered loan forbearance to about 8 million Americans.

The Trump administration’s Education Department argued that this ruling should also extend to other income-based repayment plans, including income-contingent repayment and Pay as You Earn, leaving those options uncertain.

In response, the American Federation of Teachers, which represents 1.8 million members like teachers, healthcare workers, and public employees, sued the Trump administration to reinstate debt cancellation.

What’s an income-based repayment program?

According to the National Consumer Law Center, over 13 million Americans depend on income-based repayment plans for their student loans.

These plans typically determine a borrower’s monthly payment as a percentage of their discretionary income, generally between 10% to 15%.

Most income-driven repayment plans can lead to the forgiveness of any remaining debt after 20 or 25 years, which is appealing since there are no income limits associated with them.

How will repayment programs shift under the Republicans’ ‘Big and Beautiful’ bill?

The proposed “big and beautiful” tax and spending bill by Republicans aims to phase out income-contingent repayment and Pay as You Earn by July 1, 2028. It’s estimated that these two programs have over 2.5 million participants.

If passed, millions of low- and middle-income Americans could be removed from the SAVE program, which bases monthly payments on 10%, 15%, or 20% of discretionary income.

The replacement plan from the Trump administration, termed the Repayment Assistance Plan, is set to roll out in July 2026. It proposes monthly costs between 1% and 10% of disposable income.

One key concern is that these new plans don’t have payment caps, which means many borrowers might face higher payments than before.

A summer analysis from the research nonprofit Student Borrower Protection Center warned that typical monthly payments could soar by hundreds of dollars under Trump’s new plan.

According to Sandberg, borrowers could apply for balance forgiveness after 30 years under this new framework.

Another option remains the standard plan, where borrowers commit to fixed monthly payments that pay off the loan over a period ranging from 10 to 25 years.

“If you go with a standard 10-year plan, you’ll likely end up with the highest monthly payment,” Sandberg explained.

Under this setup, loans must be paid in full, and there’s no opportunity for debt cancellation.