Rethinking Retirement Income Strategies

Many average investors limit their ideas for retirement income to the exchange-traded funds (ETFs) they see on television. But perhaps it’s time to reconsider.

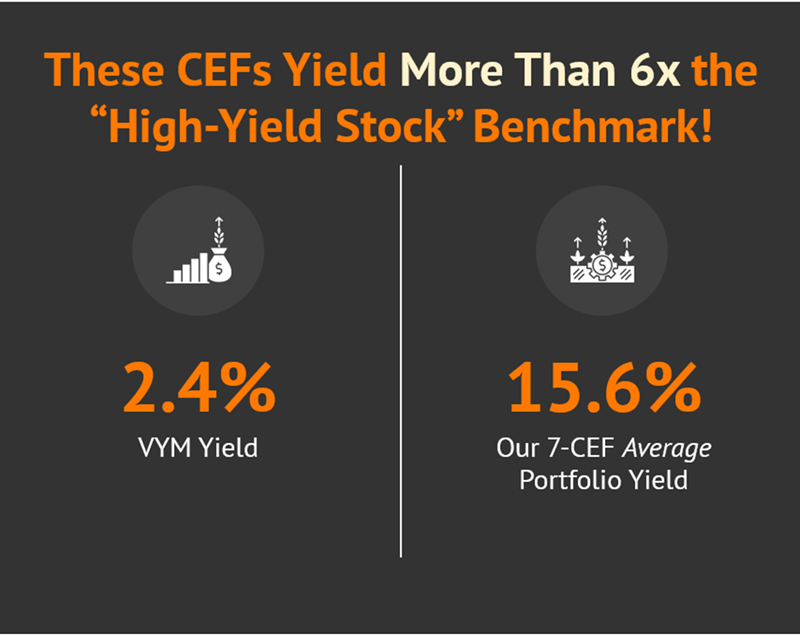

The yields on these mainstream ETFs are often around 1% or 2%. So, let’s be real—only if you have a $10 million nest egg is that sufficient for a comfortable retirement.

There are undoubtedly better opportunities out there. We can discuss funds that offer dividends of 9%, 10%, even 11%. Think about it: that’s $55,000 a year from a $500,000 investment. Now, that’s more appealing.

These alternative funds are typically actively managed, sometimes providing better custodianship than the larger, automated ETFs, which often focus more on marketing than performance.

We’re leaning toward “CEFs,” or closed-end funds, instead of those traditional ETFs because they offer substantial dividends and a more thoughtful approach to portfolio construction.

CEF, while perhaps less familiar than mutual funds or ETFs, comes with unique advantages, like:

- Regularly trading at a discount to net asset value (NAV)

- Utilizing leverage to enhance returns

- Generating cash through trading options

- Having private equity stakes

Honestly, one of the main draws of CEFs is their very high yields. Today, we’ll explore seven CEF portfolios that could yield up to $78,000 on a $500,000 investment—far surpassing what you’d see from a traditional “high-yield” ETF.

However, just like any traditional investment vehicle, a bit of homework is essential before diving into a closed-end fund. It’s important to evaluate what these CEFs are really yielding.

First, let’s look at two bond funds from a prominent asset manager: BlackRock (BLK).

Take the BlackRock Core Bond Fund (BHK, distribution rate 9.3%). Not groundbreaking, but it provides access to a broad range of investment-grade credits, U.S. government bonds, securitized bonds, and agency mortgages. It generally maintains high credit quality, even if about a quarter of the fund might carry a “junk” rating. As of now, it trades less than 4% below NAV.

This portfolio looks long-term, with an average maturity exceeding 20 years. So, it’s understandable that Fed easing has had little effect on BHK in recent years. If interest rates drop, it could be positioned favorably, but the notable leverage of 33% also makes it a higher-risk option.

On the other hand, the BlackRock Multi-Sector Income Trust (BIT, distribution rate 11.3%) offers a more benign profile despite having a “junkier” portfolio. Half of its assets are in high-yield companies, while the rest is more stable. With an average maturity of 13 years, it has less volatility than BHK and shows stronger long-term productivity.

BIT is also closer to NAV, currently trading at 95 cents on the dollar, and has shown stable income with controlled distributions since its inception in 2013.

Next, let’s shift to some equity-focused CEFs. The Neuberger Berman Next Generation Connectivity Fund (NBXG, distribution rate 9.9%) offers nearly double-digit distributions drawn from a diverse range of tech and consumer stocks. It’s an investment in the future of connectivity, but its top holdings reflect a certain lack of creativity, focusing heavily on major tech players.

Investors have shown some dissatisfaction, particularly given that NBXG trades at a 13% discount to NAV, meaning it’s fetching just 87 cents on the dollar.

From connectivity, let’s pivot to healthcare with the abrdn Healthcare Investors (HQH, distribution rate 12.1%). Despite the name, it heavily leans towards biotechnology. Two-thirds of its holdings are in biotech, while the rest spans pharmaceuticals and medical devices. Interestingly, it doesn’t use leverage, and the higher distribution rate comes from a managed policy.

However, many of its holdings yield low returns, so the dividend springs from capital gains and proceeds from options trading. Therefore, it’s reliant on stock prices increasing over time, and recent performance hasn’t been spectacular.

Oxford Lane (OXLC, distribution rate 33.5%) is quite a different beast, primarily investing in debt and equity parts of collateralized loan obligations (CLOs). Think of CLOs as pooled corporate loans, similar to mortgage-backed securities. However, the structure can be risky; they sit at the bottom of the cash flow waterfall, meaning they get paid last.

This high distribution looks attractive but should be viewed with caution; investing in OXLC is more of a gamble due to the lack of transparency surrounding CLOs.

Also, when considering OXLC’s history, you might be tempted by high volatility for returns similar to a basic junk fund.

Now, let’s look at the India Fund (IFN, distribution rate 16.1%), which is more appealing. It comprises around 50 large-cap stocks, mainly in Indian financial institutions like HDFC Bank and ICICI Bank. Given the stronger potential for Indian equities in 2026, it could really capture gains better than traditional ETFs.

Currently, IFN trades at nearly an 8% discount to NAV, or about 92 cents on the dollar, making it an interesting option.

Finally, there’s the abrdn Income Credit Strategies Fund (ACP, distribution rate 17.1%), which yields reasonable returns from a mix of global companies’ junk bonds. This fund includes approximately 150 bonds, primarily from the UK and US, with a significant portion classified as B-grade.

Even with about 30% leverage, ACP manages to offer decent returns, although its performance is somewhat moderate. That said, when priced right, ACP can show sharp market reactions—something to keep in mind for your trading strategy.

One fund I find particularly worth noting is one that pays an attractive 11%. I believe it’s a must-have for investors, especially with 2026 around the corner. The upcoming year should see increased market volatility, and this solid, growing fund could really stand out.

The monthly dividends this fund offers are stable, and there are even additional special dividends for shareholders. It’s a win-win scenario.

Overall, the manager of this fund is well-regarded in the fixed-income arena, adept at identifying opportunities that passive index funds might miss.

This fund not only provides an 11% dividend; it has the potential to grow as well. That’s why I feel strongly about including this in your portfolio, especially as the new year approaches.

For anyone interested, I’m prepared to share detailed insights on this fund. Don’t hesitate to reach out for more information.