Direct Health Care Payments: The White House’s Proposal

The White House has once again expressed its backing for providing direct benefits to households aimed at covering healthcare costs. This idea has been a significant focus for President Donald Trump for several months now.

However, health policy experts consulted by CNBC have raised doubts about this proposal. Gerald Anderson, a health policy and management professor at Johns Hopkins, remarked, “I think that’s a bad idea.” His skepticism reflects broader concerns about the idea’s viability.

The proposal is part of a broader plan introduced by the White House, which aims to reduce drug prices and insurance premiums. During the unveiling of what has been characterized as the “Great Health Care Plan,” President Trump urged Congress to adopt the framework without delay.

Enthusiasm Amid Skepticism

President Trump has shown significant enthusiasm for direct payments in his second term, even suggesting tariff dividend checks. Yet, many experts find it challenging to gauge the potential impact of the proposed healthcare payments due to a lack of critical details, like eligibility criteria and how the funds would be disbursed.

Essentially, Anderson believes that the proposal may fall short in providing consumers with financial assistance equivalent to their current support. This gap could lead to many individuals dropping their health insurance, consequently raising premiums for those who remain enrolled.

Similarly, Nick Fabrizio, a health policy expert at Cornell University, emphasized the need for robust guidelines regarding the spending of healthcare funds. “I feel very strongly that if you give people money—unless it’s like a voucher—they’re going to use it for things other than health care,” he pointed out.

Nevertheless, Fabrizio acknowledged that Trump’s broader policies on increased price transparency in the healthcare system could be beneficial in curbing costs.

Impact on ACA Subsidies

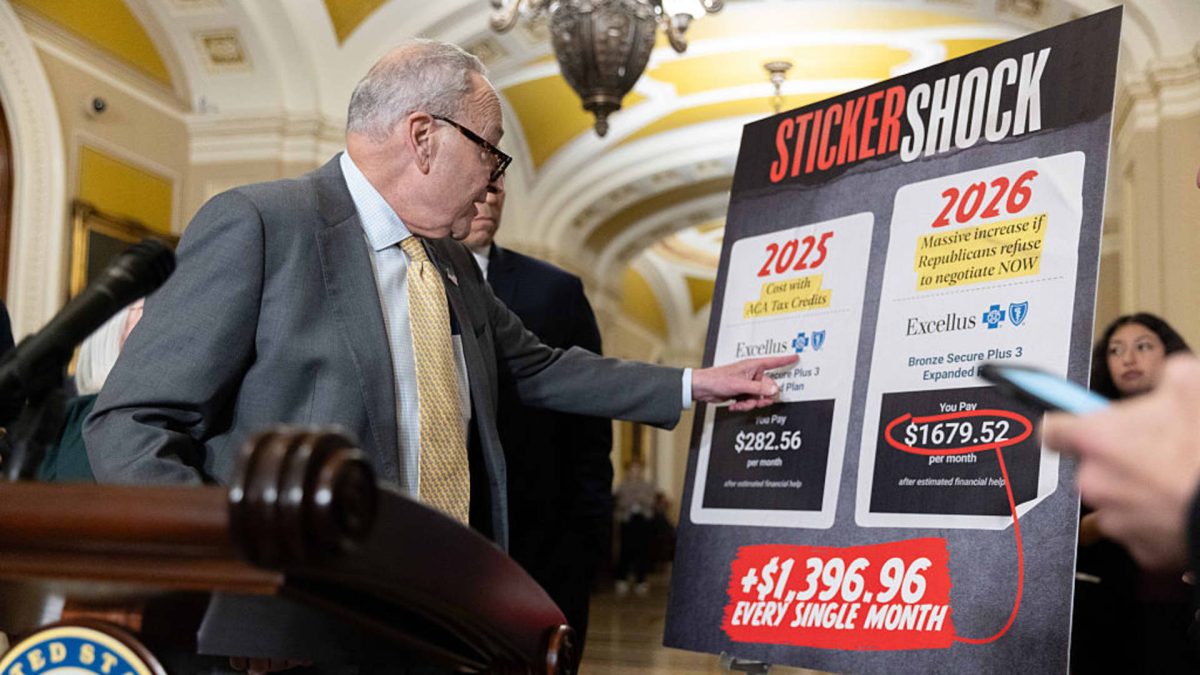

The new proposal coincides with ongoing Congressional debates regarding the renewal of enhanced subsidies that lower premiums for millions enrolled in the Affordable Care Act (ACA). These enhanced subsidies, which have been in effect since 2021, expired at the end of the previous year. According to KFF, a nonpartisan health policy research organization, this expiration could result in premiums more than doubling for average recipients.

Without these enhancements, ACA enrollees are still eligible for a baseline subsidy known as the premium tax credit. Consumers can choose to receive these tax credits either as a lump sum during tax season or through immediate reductions in monthly premiums. In the more common option, the federal government pays subsidies directly to insurance companies, which subsequently lower consumers’ upfront premiums.

Details and Challenges Ahead

Trump’s healthcare plan also proposes ending considerable taxpayer-funded subsidy payments and replacing them with direct funds aimed at helping eligible Americans purchase their own health insurance. Yet, experts remain uncertain about the operational aspects of such an initiative.

There have been past discussions among Trump and some Republicans about eliminating certain ACA subsidies in favor of health savings accounts (HSAs). While HSAs can cover specific medical expenses, they currently cannot be used for insurance premiums, thereby complicating accessibility for many consumers.

Matt McGaw, an ACA policy analyst, noted that retaining the restriction on HSA premium payments could present additional challenges for people trying to obtain insurance. He commented, “It doesn’t really alleviate many symptoms. It’s a burden for those people.”

Remaining Questions

Experts have pointed out that critical details, such as the specific amount for direct payments and potential reductions in the premium tax credit, remain unspecified. Anderson warned that if the payments are insufficient, younger and healthier individuals might drop their insurance, leading to an older and sicker insurance pool. Since those demographics typically require more medical care, insurers may then feel compelled to raise premiums.

A bill introduced in December by various Senate leaders proposed annual HSA contributions of $1,000 for individuals aged 18 to 49, and $1,500 for those aged 50 to 64. McGaw remarked that this amount is significantly less than what many enrollees, particularly older individuals, previously received through enhanced ACA subsidies.

For instance, a 60-year-old making around $63,000 annually will lose ACA subsidy eligibility and be burdened with full premiums, estimated at about $15,000 in 2026. This contrasts with the previous $7,300 subsidy received in 2025, illustrating the substantial disparities in support tied to age, income, and location.