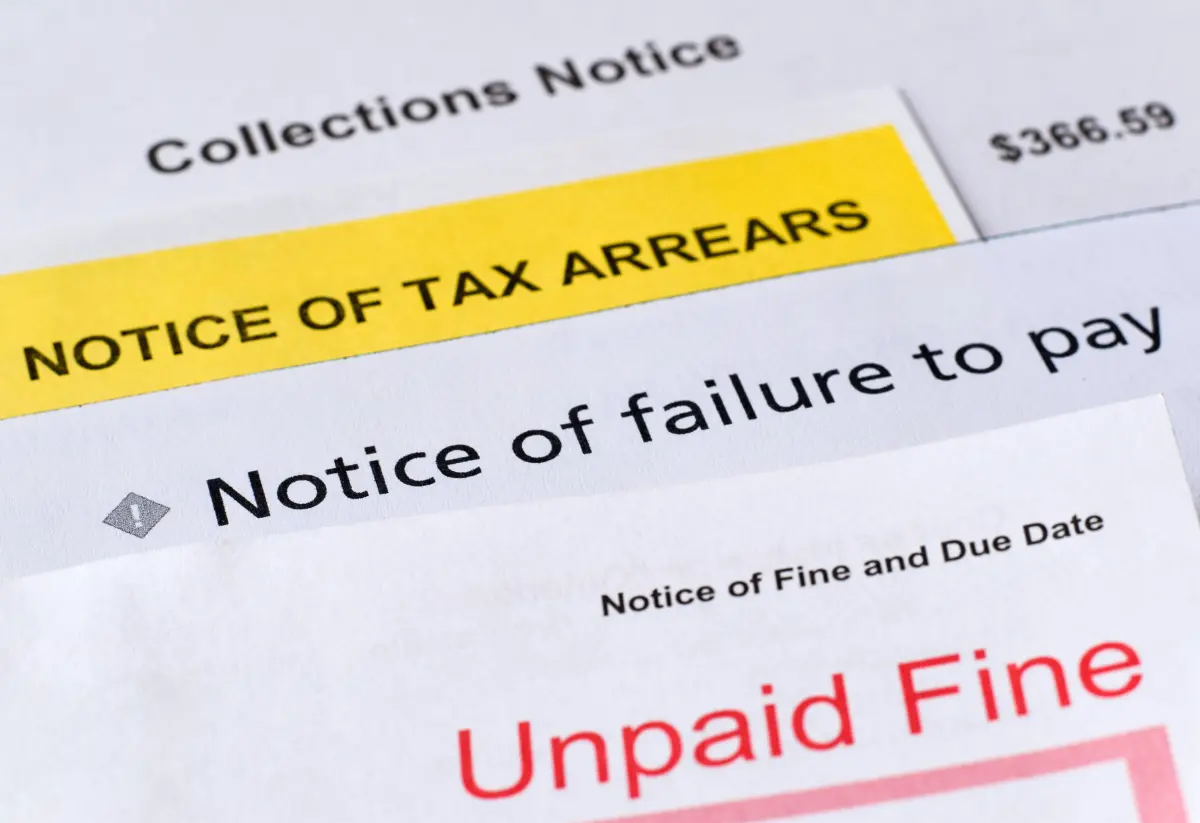

If you have a stack of unopened letters from the Treasury, it might be time to reconsider your approach. Ignoring them isn’t going to help; in fact, you’re just prolonging the inevitable.

Let’s be real: managing finances right now feels like a tight squeeze. Groceries are costing more, and tax season is right around the corner. But the IRS isn’t interested in your specific financial struggles—like a broken down car or rising rent. They want what’s due.

The government has the legal power to directly take money from your paycheck, and that’s a little scary. However, there’s a strange truth about the IRS: they sometimes feel like they’re chasing shadows.

If your debts far exceed what you can actually manage, when you talk to someone at the IRS, it often morphs into a negotiation: “What do you owe?” to “What can we realistically extract from you?” There are relief programs available that can actually lessen or pause your debt, but you need to navigate the red tape smoothly.

That’s where consulting a tax relief expert, like TaxRise, comes into play. It could mean the difference between starting fresh and facing garnished wages. Understanding those specific IRS eligibility criteria is far more crucial than those daunting figures on your bill.

So, how does this system work, really, and what can you do to alleviate some financial pressure?

What if we made the taxman disappear?

Just turning a blind eye only raises costs more. Seriously.

- Penalties and interest: The moment the deadline’s missed, the clock starts ticking. Unfiled returns and missed payments can add hefty fees that rack up daily. If you avoid it, what began as a modest tax bill could easily balloon.

- Collection action: Initially, the IRS will send a warning letter. Ignore it, and they can turn up the heat. They may garnish your wages, taking money directly from your paycheck. In serious scenarios, your bank account might even be frozen.

- Tax lien: This is a federal claim on your property. It can wreak havoc on your credit score, making it nearly impossible to sell your home or secure a loan.

IRS Lifeline: Programs that can reduce or suspend debt

The IRS recognizes that they can’t squeeze blood from a stone. They’ve set up programs for unpaid taxes, some that can erase debt, while others aim to simply halt the bleeding.

- Offer in Compromise (OIC): This is what many view as the ‘holy grail’ of tax relief. It allows you to settle your dues for a lesser amount if paying in full isn’t possible. The IRS assesses your “likelihood of collection.” If your income is low and you’re suffering genuine financial hardship, you may qualify. Just know that the process is thorough, and acceptance isn’t guaranteed.

- Currently Not Collectable (CNC) Status: This is like hitting a pause button on your financial obligations for those who can’t cover basic living costs. While your total debt remains, aggressive actions will cease until you’re in a better spot.

- Installment agreement: This sets up a monthly payment plan. Many with debts within certain limits can qualify. While it won’t reduce the overall amount owed, it does offer some relief from aggressive collection attempts.

- Reduced penalties: This can eliminate penalties but not the actual tax due. If you have a clean record with the IRS, often just asking can grant you “initial penalty relief,” particularly in cases of hardship.

- Innocent Spouse Relief: If your spouse hid income without your knowledge or made grave errors on a joint return, this program could absolve you of the confusion.

Reality check: Who fits the bill?

The IRS sticks to the numbers and won’t be swayed by sob stories. They will scrutinize your current income, acceptable living costs, and available assets.

The golden rule: If your earnings are low while expenses are high, you may have a good shot at relief. On the flip side, a hefty savings balance or luxurious items at home can significantly diminish your chances for any debt reduction. The government expects you to convert such assets into cash before they will reduce any tax losses.

How to apply (without tripping yourself up)

Securing relief involves adhering to their intricate rules.

- Submit a tax return post-deadline. Make sure you’re fully informed about the requirements before applying. If there are any years you haven’t filed, your application will be tossed.

- Select your battle wisely: If you’re making $150,000 a year, applying for an Offer in Compromise isn’t a smart move. Assess what you can realistically pay.

- Gather your receipts. You’ll need comprehensive documentation, including proof of income and a breakdown of living expenses and assets.

- Prepare for a wait: The bureaucratic process is notoriously slow. Expect the review process to drag out over several months.

Be wary of scams. The tax relief sector can have its share of predators. If a company offers to settle your debt for “pennies on the dollar” before reviewing your financials, they’re likely deceiving you. Also, if someone pressures you for immediate payment via a prepaid gift card while making police threats, you can be sure it’s a scam.

Conclusion

While the IRS wields formidable collection power, it also establishes safe options for those unable to pay. Ignoring these matters could lead to frozen accounts and lost wages.

Evaluate your relief options, ensure all necessary tax returns are filed, and if handling this feels too daunting, consider reaching out to a trusted firm like TaxRise to negotiate with the government on your behalf.

Quick FAQ

Can you actually settle your IRS debt for less than what is owed?

Yes, but only via programs like the Offer in Compromise, and you’ll need to demonstrate clear financial hardship.

Will the government ever fully forgive tax debt?

Complete forgiveness is quite rare. Typically, they may offer lower fines or settle for an amount based on what you can afford.

Do I have to hire a tax professional to handle the IRS?

While it’s possible to manage the paperwork on your own, hiring a CPA, tax accountant, or professional relief company is generally wise if your situation is complex or if your debt is significant.