Market Perspective Amid Ongoing Iran Conflict

While a resolution to the Iran war seems distant, it may not be wise for investors to hold off on making moves.

What if negotiations don’t lead anywhere? Could inflation surge? Should you just hang back until this all blows over? These are valid concerns circulating as this conflict continues, but waiting could come at a significant cost.

Since my last update in March, the U.S. has escalated its blockade in the Strait of Hormuz. Yet, the situation remains largely unchanged. This blockade primarily targets Iranian imports and exports. Most of Iran’s oil is directed towards China, which has already built up significant reserves.

At the same time, alternatives to the strait are emerging. Before the conflict, Saudi Arabia’s East-West pipeline saw exports of less than 800,000 barrels per day. Now, that number has soared to over 5 million. Similarly, exports from Abu Dhabi’s Fujairah port surged by 40% in March, reaching 1.6 million barrels per day, allowing Gulf oil to skip the Strait altogether.

This situation applies even to jet fuel. The dire forecasts involving mass cancellations and inflated airfare hinge not just on the Strait remaining blocked, but also on whether other supplies are available. China is reviving its exports, and various refineries are ramping up production. The EU’s strategic decisions concerning U.S. kerosene have eased concerns about disrupted summer travel. The world is, understandably, adapting.

Outside the Gulf, energy-producing nations are stepping up their game. U.S. oil exports recently reached an all-time high in April. Venezuela is also increasing its transportation efforts. Nations dependent on Qatar’s natural gas, like South Korea and Italy, are turning to additional supplies from the U.S. and Australia. Even Asian countries are reigniting coal-fired power plants. Any looming energy shortages are likely to be brief.

There’s been some chatter about Tehran potentially imposing a toll of $1 per barrel for passage through Hormuz, accounting for roughly $2 million per ship. However, given that the marginal cost of Gulf oil sits around $20 per barrel, an extra dollar shouldn’t be a game changer. Interestingly, a Japanese tanker managed to pass freely on April 29. Could this open up possibilities for more similar instances?

If Iran has indeed set up a toll system shaking up prices, it might just be a temporary blip. Should prices rise, other global supplies will likely increase as well, driving costs down eventually. It’s a cycle that tends to play out consistently.

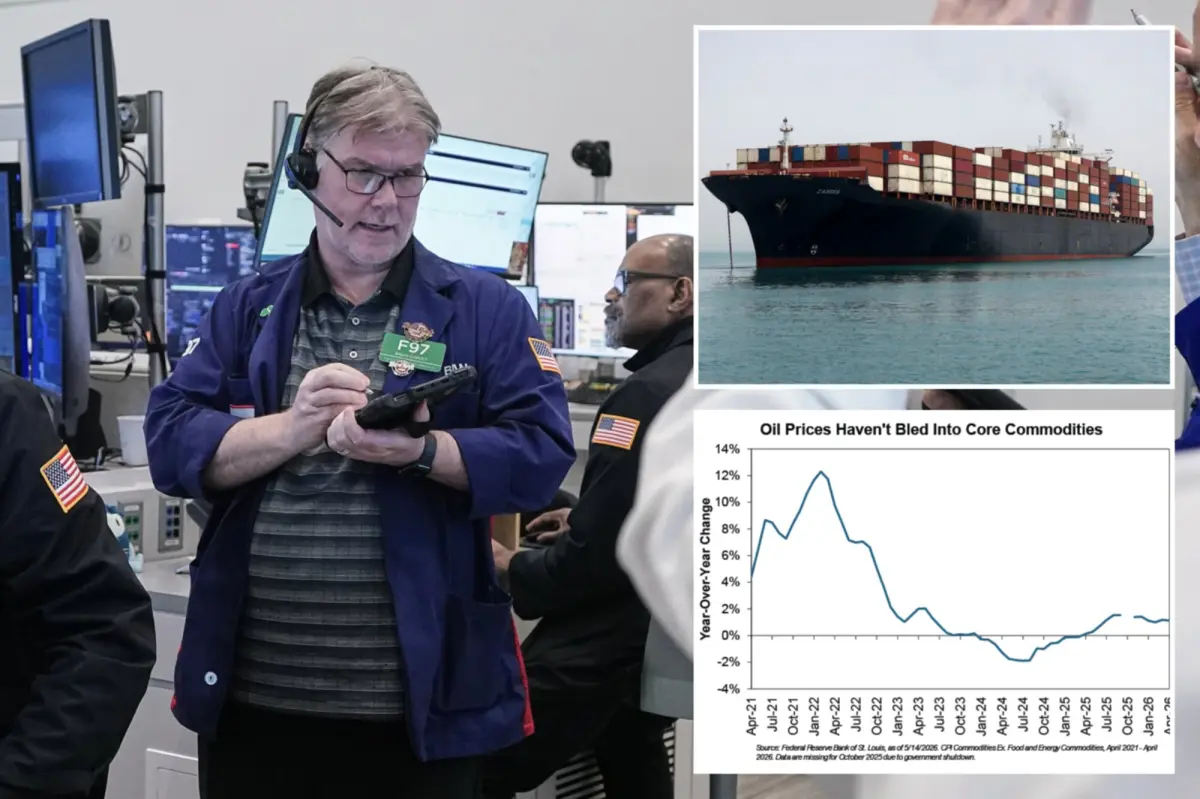

This also alleviates inflationary worries. Yes, U.S. consumer inflation hit 3.8% year-over-year in April, attributed to climbing fuel prices. But this doesn’t imply the kind of distress seen in 2022. Nobel laureate Milton Friedman highlighted that inflation fundamentally emerges from excessive money creation, wherever it occurs. The broadest measure of U.S. money supply, M4, grew by 5.8% year-over-year, aligning well with pre-pandemic levels and falling short of the over 30% surge during the pandemic that fueled rampant inflation in 2022.

A meaningful escalation in the money supply is crucial for energy price hikes to instigate inflation. Higher energy costs may challenge luxury brands as they cope with steeper fuel expenses, but this won’t necessarily inflate overall prices or hamper GDP significantly. It’s more of a redistribution of spending. Plus, energy comprises only about 6% of the consumer price index in the U.S.

Concerns have been raised about supply chain impacts, especially for petrochemical materials tied to plastics and fertilizers, sparking potential price increases across various sectors. However, that’s not quite materializing. Excluding energy and food, U.S. commodity prices rose just 1.1% year-over-year in April, easing from 1.2% in March and remaining flat compared to earlier months. Concurrently, trucks are moving backlogged fertilizers from the Gulf, alleviating shortages.

So, is there a rationale for delaying stock investments until the situation stabilizes? The market historically doesn’t wait for full clarity. Take 2022, for example. U.S. stocks hit their lows in October amid escalating Ukraine conflict, a 9.1% inflation rate, and interest rate hikes. Yet, stocks were already pricing in a brighter future much earlier than expected, mirroring behaviors observed post-coronavirus and after last year’s tariff shocks.

We’re witnessing a similar scenario now. Stock prices have rebounded to historical highs, demonstrating a pattern where they rise ahead of sentiment recovery. Fear can be a costly emotion for those seeking clarity.

There may undoubtedly be challenging twists ahead. However, the market typically shifts focus away from daily fluctuations over time. It’s best to detach from daily news about blockades, threats, and protracted negotiations. Instead, like the stock market, it helps to look further into the horizon.