Quality investment is a mystery. If so, investment strategies rarely increase profits without increasing (or reducing) risk. But the quality factor has done just that over the past decade.

Higher risk-free returns are counterintuitive and undermine economic theory in financial textbooks. What's even more inexplicable is that there is no universally accepted definition of quality or consensus that the metric best identifies it.

Three questions may help to solve these mysteries:

- What is quality?

- Why does it work?

- How is it captured?

Define quality investments

Quality is in the eyes of the viewer. Just as all of us rattle our own standards about why we make our products high quality, investors on high quality companies were able to do so.

How scholars and investors combine and match quality characteristics is another story. Eugene Fama and Kenneth French have incorporated quality by expanding the three-factor model (market risk, value, size) and five factors (to address profitability and conservative investments). It is intuitive to buy a profitable company that does not require large investments to grow its profits. Robert Novie Marx put it to him Original work on profitability “Traditional value strategies fund the acquisition of cheap assets by selling expensive assets, while profitability strategies leverage different aspects of value and sell unproductive assets to make them productive by selling non-productive assets. We will fund the acquisition of assets.”

2018, Research by Jason Hsu, et al.looking at many definitions of quality, we finally found evidence that the following indicators provide excellent performance.

- Profitability

- Accounting quality

- Payment/Dilution

- Investment – A note that other factors in the multifactor model can explain the edge.

To expand on the Novy-Marx explanation above, quality companies have productive assets that can be reliably explained in their financial statements and are not diluted by companies issuing new shares.

Why do high quality investments work?

If the market is very efficient, quality won't work. The quality factor risk premium means that these companies are always at low prices. How can it happen across the region and over a long period of time?

Antti Ilmanen, global co-head of systematic investment Titan AQR's portfolio solutions, called out some behavioral biases and explanations on why quality works in his book. Investing despite low expected returns. They include investors' preferences for stocks that function like lottery tickets, constraints on leverage, and “story-oriented” analysts/investors.

- Lottery, or potentially high-return stock preferences, stand at the central stage of markets driven by crypto, meme stocks, and funds traded on leveraged solo exchanges. Buying Bitcoin for 10 years ago was like winning a lottery. Gambling mentality will help some investors take a greater risk in the hope that they will more easily (and safer) compound things with quality factors. I encourage them to.

- Some investors may not be able to use leverage. That constraint shifts focus from risk-adjusted returns to total revenue, pushing them up to risky assets, leaving high-quality companies behind.

- Story-oriented analysts and investors buy stories rather than fundamentally healthy business. This usually excludes high-quality stocks from your portfolio.

Add my own thoughts to the mix: Quality works as investors are looking for a core/satellite portfolio. The broad market funding forms their core holdings. They are unlikely to add funds with similar holdings and returns. The quality factor ETF fits that type. They often own many of the large stocks that dominate the market, so it makes sense for investors to seek a more differentiated strategy for satellite locations.

Find a quality ETF

The definition of quality is not just a contradiction that investors need to grasp. Academic and fund providers will leverage different quality metrics, even if they want the same characteristics, such as profitability.

Novy-Marx has discovered one measure of profitability: the company's gross profit/assets. [(revenue – cost of goods sold)/assets]- Historically, it has the same predictive power as a price/book. Better yet, gross profit tends to be negatively correlated with value. This means that combinations need to diversify and reduce volatility while leveraging two powerful factors.

Cliff Asness and his colleagues from AQR Published research This showed that “quality negative junk” factors improved performance in traditional factor regression. High Quality Negative Junk combines several metrics that fall into three buckets: profitability, growth and safety. AQR quality interpretations were averaged by Novy-Marx's total profitability with share return, asset return, cash flow on assets, and gross profit. Growth metrics aggregated the rate of change for those same profitability metrics. And they took advantage of safety, low beta, low leverage, low bankruptcy risk and low ROE volatility.

HSU and the Researcher Team We also tested quality metricsadded the aforementioned rate of return on profitability, exceeding dozens more under the themes of revenue stability, capital structure, profitability growth, accounting quality, payment/dilution and investment. Roughly, their studies proved profitability, accounting quality, and investment metrics were robust in regression tests, but not increased profitability, capital structure, and revenue stability metrics. I understand.

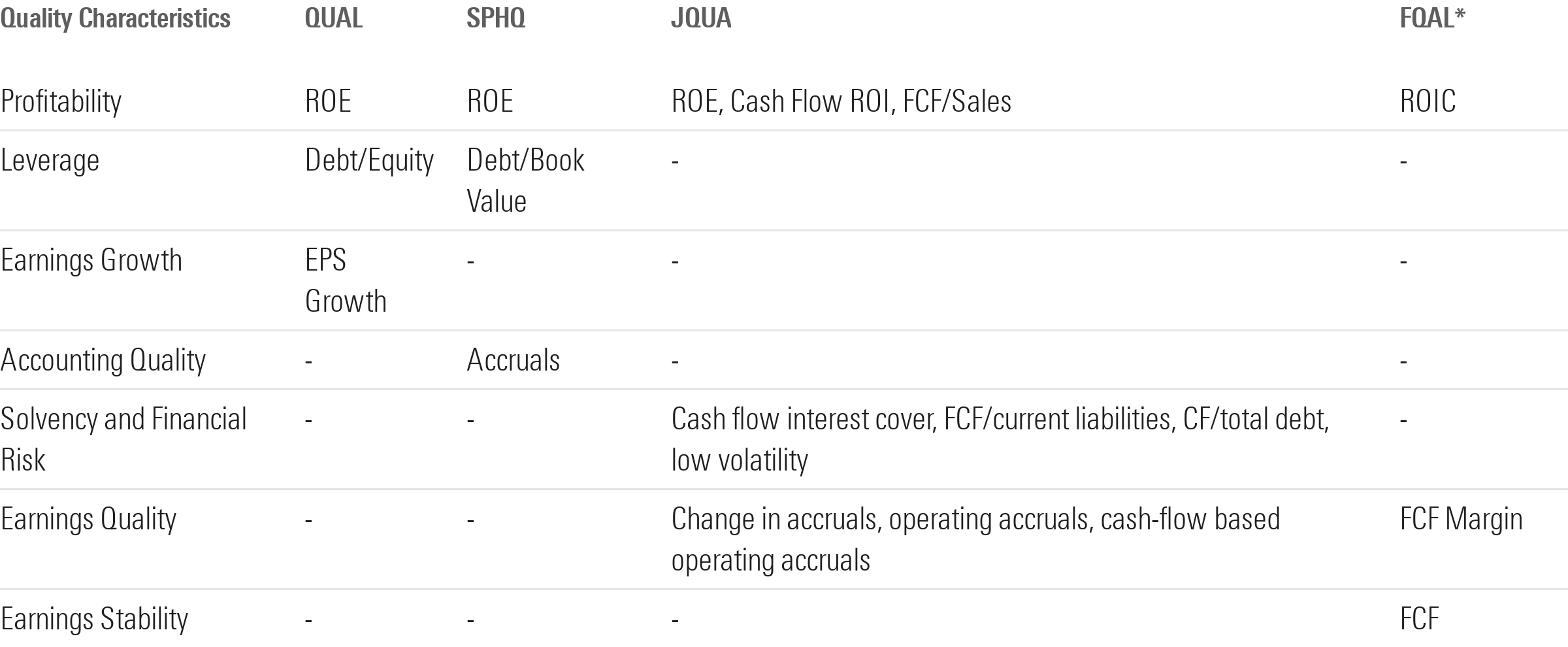

So how did practitioners make this study work? Of course, it's not consistent! The following two exhibits demonstrate the approach taken by four ETFs, focusing on quality. Interestingly, at least one of financial leverage, revenue growth, or revenue stability led it to each of these ETFs despite the findings of a study by HSU. These ETFs went to the bottom of the company's income statement by deriving net profits from the ROE metric, rather than the novelist approach of reducing accounting noise using the top figures in the income statement. .

Which ETF is best matched with quality factor studies? To test this, we performed regressions using the Junk model minus the AQR quality and the FamaFrench 5-factor model (with integrated total profitability and investment).

Fama and French's Model, Investco S&P 500 QualityETF SPHQ made the most of its quality through a combination of profitability and investment. According to AQR's model, the Invesco S&P 500 quality ETF was the only ETF with a quality factor that was not statistically important. The quality metrics (ROE, accrual, debt/book price) of the Invesco S&P 500 Quality ETF conceptually match some of the junk definitions (less profitability and safety, growth) minus the quality of AQR Considering this, this is somewhat surprising.

ETFS's diverse approach to portfolio construction failed to mark many regression results. iShares MSCI USA Quality Factor ETF Qual uses sector-neutral weighting. The Invesco S&P 500 Quality ETF focuses on top 100 S&P 500 companies, using quality definitions and weights. JPMorgan US Quality Factor ETF JQUA has just 18% of its assets in its top 10 shares, with its 280 holdings and only 18% of its top 10 shares, and its average market capitalization is smaller than other quality ETFs, so it has the best portfolio of bundles. Fidelity Quality Factor ETF FQAL also takes a sector-neutral approach, holding roughly the same number of stocks as the quality factor ETF of ISHARES MSCI USA, but only 50 out of 125 holdings due to different definitions of quality is duplicated.

Despite the differences, strong performance has put together these four ETFs. From December 2017 (the earliest month in which all four ETFs were live) to September 2024, four ETFs matched or defeated the Morningstar US Market Index with risk-adjusted returns.

The JPMorgan US Quality Factor ETF and the Investco S&P 500 Quality ETF top the list in total returns and have the lowest volatility (quality enigma lies). Only faithful quality factors delayed market returns over that period, and the quality factor ETF of iShares MSCI USA was the only ETF with higher volatility than the market.

How ETF Investors Use Quality

The quality remains a bit of a puzzle. The divergent approach by scholars and practitioners leaves some questions unanswered. However, the quality ability to beat the market with low volatility will continue to be valuable in tracking.

Each quality ETF offers a version of quality for investors, but incorporating quality can be useful for any strategy. Top rated dividend ETF control for quality to avoid the pitfalls of chasing yield. Many ETFs offered by Dimensional and Avantis explicitly utilize profitability in combination with value and small size. There are many options for investors, and it's wise to incorporate quality in some way. To be precise, how does it stay in the eyes of the viewer?

This article was first published in the October 2024 issue Morning Star etfinvestor. Download a free copy of Fundraiser by Visit this website.