-

Palantir Technologies had an impressive performance in the S&P 500 and Nasdaq-100 over the past year.

-

The company’s excitement about artificial intelligence (AI) has pushed its stock prices up significantly, but investors might want to closely examine its valuation trends.

-

The last couple of years have seen a surge in AI focus, particularly as large tech companies have drawn much of the attention and enthusiasm surrounding the AI outlook.

-

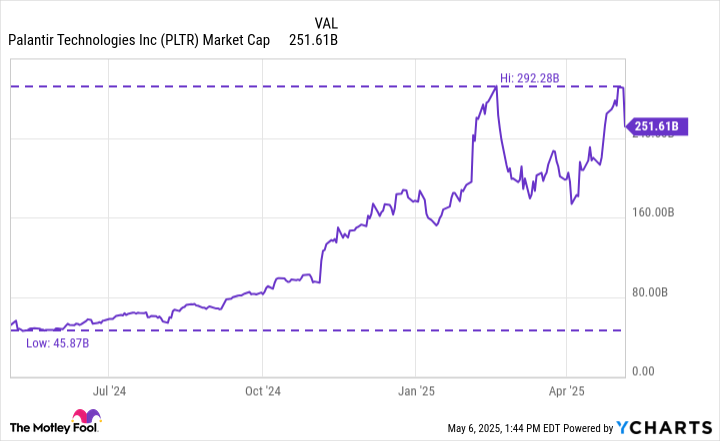

However, smaller companies have demonstrated their ability to challenge bigger players, with Palantir being a prime example; as of May 6, its stock has skyrocketed by 361% over the past year.

-

While Palantir has gained enormous popularity as an AI stock, savvy investors are questioning whether such parabolic gains can sustain themselves. It’s worth looking into the company’s valuation trends and comparing these with historical events in the tech sector to better gauge future directions.

-

In just one year, Palantir’s market capitalization has surged from approximately $46 billion to over $250 billion.

-

A few months ago, a fellow contributor analyzed valuation trends from the dot-com bubble as they relate to Palantir’s current situation.

-

Before the dot-com crash, companies like Cisco and Amazon had price-to-sales ratios that peaked around 40, similar to Nvidia during the current AI boom, which recently peaked at about 46.

-

Indeed, Palantir’s P/S ratio is now more than double that of some major tech firms during a period of market euphoria.

-

This raises concerns that Palantir’s valuation might be inflated; however, it’s critical for investors to consider the aftermath of the dot-com boom and contemporary trends to better analyze where the stock might go next.

Currently, the company holds a price-to-sales ratio of about 91, but this figure alone may not provide much insight.

At present, comparable P/S multiples for Cisco, Amazon, and Nvidia are 4.4, 3.1, and 21.6, respectively, indicating that Palantir’s ratios could face substantial compression.

While this might lead some to panic-sell, it’s important to remember that valuations can normalize over time as companies grow. Essentially, as revenues and profits increase, so too can market multiples.

Notably, a compressed multiple doesn’t automatically translate to a decline in market value. For instance, while Cisco’s valuation hasn’t recovered fully, it still has a market cap of $236 billion, highlighting that long-term stock holding can yield significant returns.

Additionally, Nvidia’s market cap has more than doubled from two years ago, despite hitting a P/S peak around 46.

What sets Palantir apart is the belief that the AI sector isn’t currently in a bubble. Its growth outlook seems clearer than that of Cisco or Amazon during the dot-com era, mainly due to rising demand for AI solutions. That said, investors should tread carefully, weighing the potential opportunity costs of entering at historically high valuations.

Historically, Palantir could justify its $250 billion market value, but there’s also strong evidence suggesting it may eventually trade at more reasonable metrics for new investors. A sound strategy for those looking to invest now would be to use dollar-cost averaging, and it might be wise to hold the stock for the long haul to maximize potential gains.

It’s crucial to deliberate carefully before purchasing shares of Palantir Technologies.