Some employers are shifting their approach to health insurance, allowing workers to decide on their own coverage. Instead of providing traditional health plans, they’re offering funds for employees to buy their own insurance through what’s known as individual coverage health reimbursement arrangements (ICHRA).

Proponents argue that this method can benefit small businesses that struggle to provide insurance. It aligns with certain political goals aimed at easing employer expenses while giving employees greater control over their healthcare choices.

That said, there are concerns about whether employees will be able to effectively navigate the insurance market—that is, having to shop for insurance can be daunting for many.

“It might not be a perfect solution, but it addresses the needs of many,” remarked Cynthia Cox from KFF, who examines healthcare issues.

Here’s a closer look at how this insurance strategy is changing.

What is ICHRA?

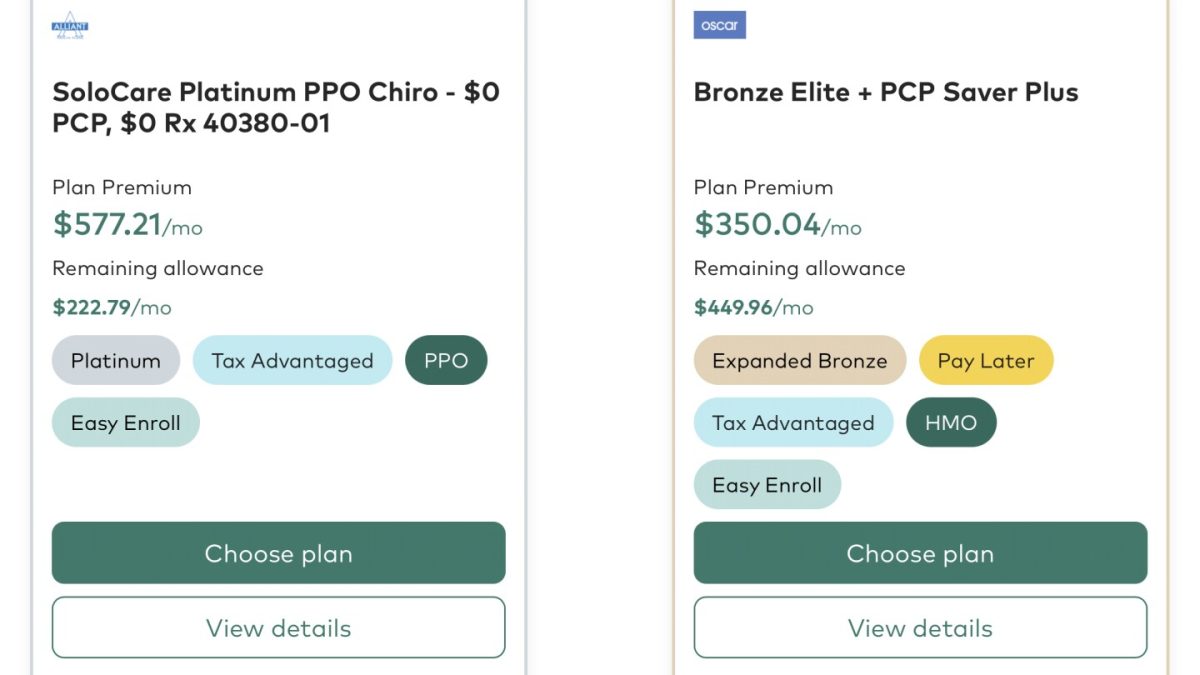

Typically, U.S. employers offer one or two group insurance plans for employees, covering most of the premium costs. ICHRA changes this by allowing companies to contribute funds while employees pick their own plans. To facilitate this, employers often partner with external firms to assist employees in making informed choices.

Introduced during Trump’s administration, ICHRA started somewhat slowly but has gained traction in recent years.

Why is ICHRA significant?

For business owners, this model provides predictable costs, taking the onus off them to manage their employees’ insurance choices.

“We’re eager to see how businesses adapt to this new process,” said Jeff Yuan, co-founder of Taro Health.

Small businesses are especially susceptible to fluctuations in insurance costs, which can escalate dramatically if key employees face significant medical issues. The ICHRA system helps stabilize these expenses.

Yuan’s company’s pricing is influenced by employee demographics, with coverage costs ranging from $400 to over $2,000 monthly.

What sets this method apart?

Unlike the limited options typically provided by employers, ICHRA presents a broader selection of individual insurance plans. This may enable employees to find coverage more suited to their needs, such as plans specifically designed for chronic conditions like diabetes.

Moreover, if employees change jobs, they may retain their insurance longer than under standard employer plans. While they would likely have to pay full premiums, keeping their coverage means less hassle in finding new doctors.

Mark Bertolini, CEO of Oscar Health, pointed out that frequent job changes are common.

“Insurance is most effective when it stays with the individual,” he added.

What challenges do employees face?

Health plans in individual markets often come with narrower networks compared to employer-sponsored insurance. This can cause complications for patients who need to see multiple doctors.

Additionally, those selecting their own insurance might feel overwhelmed by various coverage options and costs. Thus, it’s crucial for employers to assist in the decision-making process.

Brokers or tech platforms that set up ICHRAs generally help by assessing employees’ medical needs and any upcoming procedures they may have.

How widespread is this method?

There’s no solid national figure on how many individuals have coverage through ICHRA, especially among small businesses with fewer than 50 employees.

Nevertheless, the HRA Council, which advocates for these systems, reports significant growth in adoption. They collaborate with businesses to implement ICHRAs and are tracking this expansion.

This year, around 450,000 people have accessed coverage through ICHRA, marking a 50% increase since 2024. Council executive director Robin Paoli mentioned that the market could potentially double.

Still, these arrangements are a small portion of employer-sponsored health insurance overall, with KFF estimating about 154 million Americans were covered through work last year.

Will this trend continue?

Several factors might push more employers toward ICHRA. As healthcare costs rise, companies may look for ways to mitigate their financial risk.

Some proposed tax reforms could provide incentives for adopting such arrangements and are currently being debated in the Senate.

Additionally, if government subsidies that assist in purchasing individual market coverage through the Affordable Care Act roll back this year, more individuals may become eligible for ICHRA.

However, anyone currently receiving these government subsidies wouldn’t qualify for ICHRA. Brian Blaze, who served as a health policy advisor during the Trump administration, noted that “Increased subsidies can drive private market growth.”