(Bloomberg) – Bank of Japan Governor Kazuo Ueda will consider the need for a rate hike on Friday as expectations for a rate hike rise, but he won’t raise rates unless there is a market shock in President Donald Trump’s first days in the White House. We plan to consider the necessity of

While attention is focused on the pace of interest rate cuts in the rest of the central banking world, particularly the Federal Reserve, Ueda and his board are still heading in a different direction as they seek to gradually pull Japan back toward traditional policy settings. .

After decades of low prices and sluggish economic growth, Japan appears to be moving closer to achieving stable inflation with strong wage growth, allowing the Bank of Japan to lower its borrowing costs to match that of other major economies. It has now become possible to raise the level to a level that can be achieved.

About 90% of economists surveyed by Bloomberg this month said that prices and economic conditions warrant a rate hike of 0.25%. About three-quarters of economists surveyed expect the central bank to act this week. Friday's overnight swaps briefly showed that traders had almost fully priced in a rate hike in January.

Bloomberg reported on Thursday, citing people familiar with the matter, that Bank of Japan officials believe there is a good chance of a rate hike as long as President Trump does not cause too many negative surprises in the near term. . According to people familiar with the matter, some of the factors supporting this move include the possibility of upward revisions to the price outlook and expectations for steady wage increases.

The report further fueled hopes that a rate hike is near, after Ueda and his deputy Ryozo Himino said they would consider the need to raise borrowing costs at their next meeting.

Some BOJ watchers interpreted the comments as a sign that some action was being prepared as the central bank's top brass worked to clarify communication. Some analysts blame the lack of messaging for a rate hike in July for the summer meltdown in global markets.

Economists point to the yen as another factor. The currency is hovering around 160 yen against the dollar, and last year saw billions of dollars of market intervention to support the yen. If interest rates are raised, the difference in interest rates between the US and Japan will narrow and the currency will appreciate.

“Recent interest rate hike signals from Bank of Japan officials are supporting the yen. In the longer term, Japan's higher interest rates and stronger growth potential could also break the trend of yen selling.”

—Taro Kimura, Senior Japan Economist. Click here for complete analysis

So what is stopping Ueda? Economists warned that the potential market turmoil caused by Mr. Trump could give the Bank of Japan reason to wait a little longer. Widespread tariffs are a major concern for all of the United States' major trading partners, including Japan, and the next president is likely to issue a slew of executive orders on the first day of his second administration.

More information on the annual wage agreement will become available in March, as Mr Ueda seeks more clarity on wage trends that support stable price growth among potential delay factors closer to home. Meanwhile, Prime Minister Shigeru Ishiba has no guarantee that he will be able to pass the annual budget without the support of at least one opposition party, which is cautious about raising interest rates by March.

Still, given the clear signals from Mr. Ueda and Mr. Hino, and with high hopes for a rate hike, the Bank of Japan will face further questions about its communications strategy if it fails to do so this time.

Elsewhere, President Trump's inauguration will set the tone for financial markets and overshadow the World Economic Forum in Davos, where he is scheduled to speak by video on Thursday. The Purchasing Managers' Index of countries around the world in January is also attracting attention.

Click here to see what happened over the past week. Below is a summary of what will happen next in the global economy.

USA and Canada

President Trump will take the oath of office on Monday and deliver his inaugural address indoors as temperatures in the capital hit just 22 degrees Celsius (minus 6 degrees Celsius). According to Bloomberg Economics, he is expected to announce a number of executive orders shortly thereafter, including potentially reversing the Biden administration's immigration policies.

The U.S. economic calendar looks bright, with existing home sales in December and consumer sentiment data from the University of Michigan drawing attention. These reports are scheduled to be released Friday along with the S&P Global Manufacturing and Services Survey. Federal Reserve policymakers are on a blackout ahead of their January 28-29 meeting.

Meanwhile, Canadian Prime Minister Justin Trudeau huddled with his cabinet members at a retreat in Quebec during Trump's first two days in office, warning that if Trump follows through on his threat to impose steep tariffs on his country's products, We plan to make it compatible.

The race to become Canada's next prime minister has begun amid uncertainty, with former central banker Mark Carney and former finance minister Chrystia Freeland entering the Liberal Party leadership race. The Bank of Canada survey for the fourth quarter and inflation data for December will also be released.

Asia

Ahead of the Bank of Japan's interest rate decision on Friday, Japan is expected to release inflation statistics that are likely to show an upward trend, further supporting the case for rate hikes.

The Monetary Authority of Singapore held its first meeting of the year on the same day, and some economists see risks in easing measures.

Earlier on Wednesday, Malaysia's central bank is likely to extend its long-term policy suspension and keep the benchmark interest rate unchanged at 3% since May 2023 as price pressures remain manageable.

Earlier in the day, New Zealand released its all-important inflation report for the December quarter, which will factor into decision-making when the central bank meets for the first time in February this year.

Also on Wednesday, investors weighed in on South Korean household finances after consumer confidence dipped last month amid political turmoil sparked by the brief imposition of martial law that led to the impeachment of President Yoon Seok-yeol. You will gain insight into the mood.

The latest gross domestic product (GDP) estimates released on Thursday could show that South Korea's economy will recover slightly in the last three months of 2024.

This week, trade figures for the Philippines, Malaysia and Japan will also be released, while Purchasing Managers' Indexes will be released for India and Australia. Taiwan will release gross domestic product estimates on Friday.

Europe, Middle East, Africa

Davos will be in the spotlight as world leaders and financial officials mingle with business executives in the Swiss mountain resort.

European Central Bank President Christine Lagarde and other board colleagues will also be in attendance, as will Swiss National Bank President Martin Schlegel.

Embattled British Prime Minister Rachel Reeves is also scheduled to attend. His comments will be closely scrutinized given the market's focus on the country's fiscal problems.

Back in the UK, wages statistics will receive serious attention as concerns about inflation persist. Increased wage pressures are widely expected by economists, but the Bank of England should be able to cut interest rates as soon as next month.

Friday's PMI numbers will be key and provide the first signal for manufacturing and services to start the year, before President Trump reveals how far he intends to follow through on his tariff threats, both in the UK and the eurozone.

Apart from Europe, South Africa's data on Wednesday is likely to show inflation accelerating to 3.2% in December due to higher petrol prices and a weaker rand. The forward rate contracts used to estimate borrowing costs currently factor in just one rate cut of 25 basis points in 2025, likely to take effect on January 30th.

Three financial decisions are planned for the region:

-

Angola's central bank is likely to keep its policy rate unchanged at 19.5% on Tuesday for a fourth consecutive session in a bid to contain Africa's highest inflation rate of 27.5%.

-

Norwegian officials are widely expected to keep borrowing costs at a 16-year high on Thursday. They could reiterate that the first post-pandemic rate cut from the current 4.5% level could come in March, and that there is uncertainty about further easing beyond that. Most economists expect a total decline of four quarter points this year.

-

Turkey's central bank has warned that the 250 basis point interest rate cut in December does not necessarily mean the start of an easing cycle. But many economists and traders think it has, and are predicting another move of the same magnitude on Thursday, pushing the benchmark rate to 45%.

-

Ukrainian policymakers on the same day raised interest rates to 14% for the second month in a row as they seek to rein in accelerating inflation and face uncertainty over continued U.S. support in efforts to repel Russian aggression. It is expected that it will increase to

latin america

The region's two largest economies reported mid-month inflation, and both are likely to see lower inflation, but that's where the similarities end.

Analysts believe Brazil's economic slowdown in January will be temporary, before surging in February. Economists surveyed by the central bank expect monthly inflation to reach near zero in January and rise above 1.3% in February.

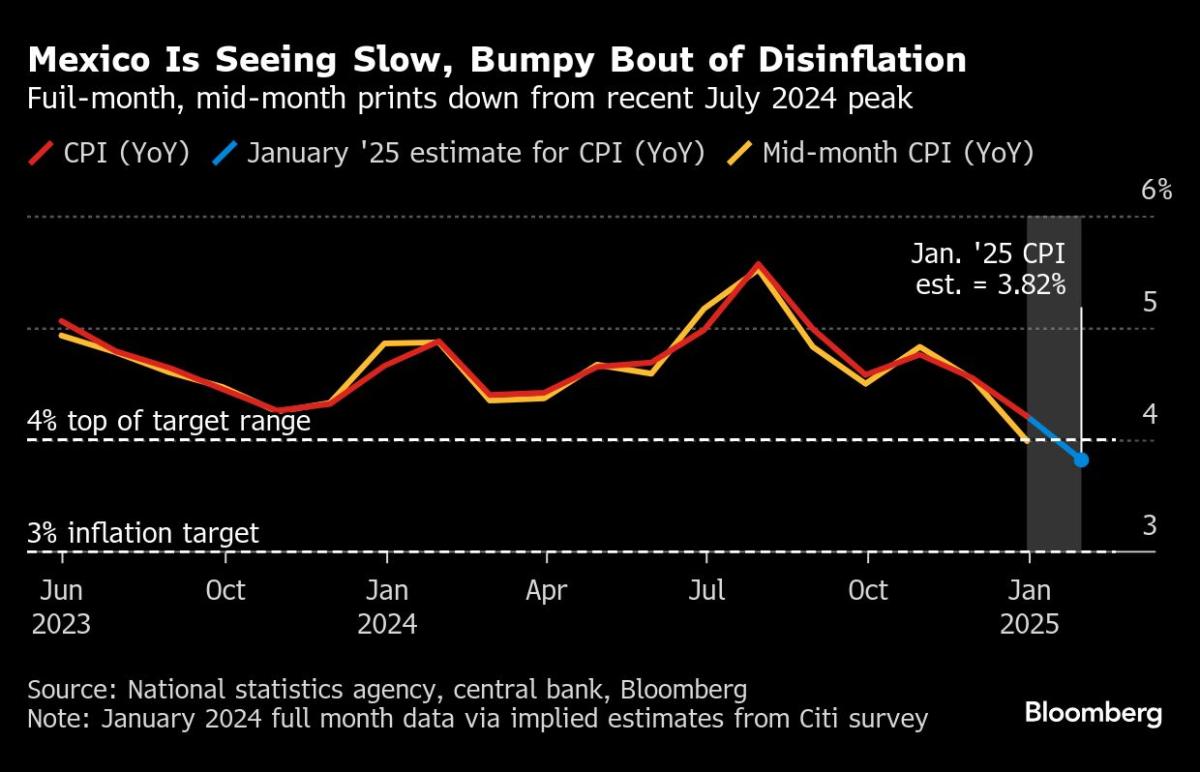

Mexico is in a precarious but undeniable position, riding a wave of disinflation due to tight monetary policy and slowing growth, with analysts surveyed by Citi predicting that the Bank of Mexico's target range of 2% to 4% It is suggested that the deceleration will be within %. Full-month and mid-month measurements for each economy are often tracked very closely.

As usual, Brazil Watcher has a new survey of central bank economists, which will be joined by a survey of Chilean central bank traders and a Citi survey of Mexican economists.

Argentina releases trade statistics for December, along with consumer confidence and monthly wage data. Colombia has released its import and trade balance for November.

Mexico, Argentina and Colombia have released economic activity data for the November end of Latin America's six largest economies.

Among this group, Brazil's economy is likely to lead the pack at the end of the year with a growth rate of over 3%, but it will relinquish its position to Argentina in 2025, with some analysts predicting up to 5% growth. % growth is expected.

–With assistance from Laura Dillon Kane, Monique Vanek, Piotr Skolimovski, Robert Jameson, Swati Pandey, Ott Ummeras, and Vince Gall.

Most Read Articles on Bloomberg Businessweek

©2025 Bloomberg LP