Palantir’s AI Boost and Stock Performance Insights

Palantir has seen significant growth thanks to favorable AI trends, leading to notable increases in its revenue and operating income for the second quarter overall.

Interestingly, despite having strong results in the first quarter, the stock faced a difficult sell-off after that report was released.

In recent months, Palantir’s shares have made a sharp recovery and are now trading at levels that are historically high—perhaps a bit too high for comfort.

Palantir Technologies (NASDAQ: PLTR) has emerged as one of the key beneficiaries of the AI boom. The company’s software solutions, Gotham and Foundry, act as foundational technology for numerous global businesses and government entities.

As of the closing bell on July 25, Palantir’s shares have skyrocketed by 110% this year. This performance places it among the best in the S&P 500 and NASDAQ-100.

On August 4, the company plans to announce its financial and operational results for the second quarter of 2025. Given the strong performance in Q2, there are some important points investors might want to consider.

Is now a good time to invest in Palantir stocks? Perhaps, but it’s worth reading further.

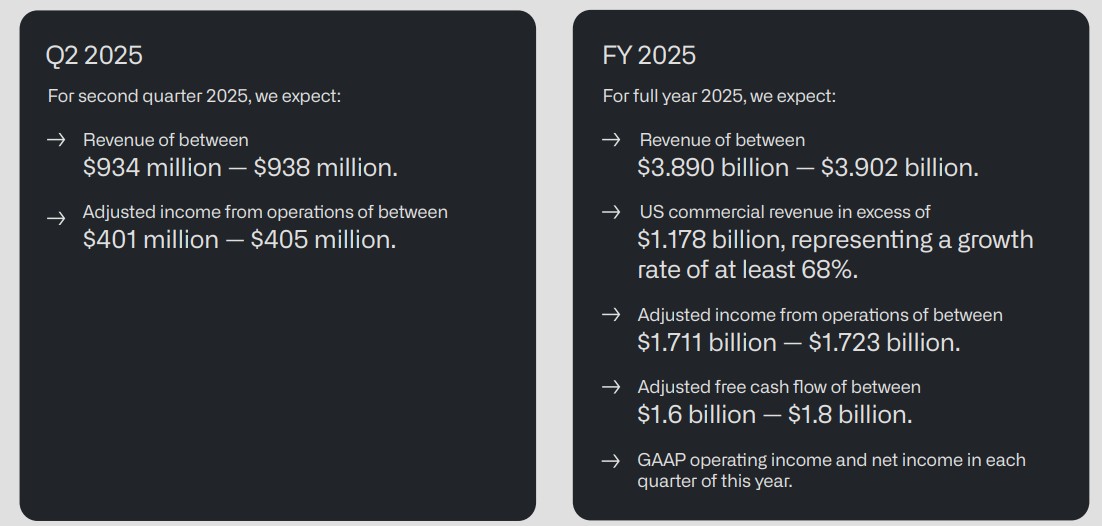

Back in May, during the first quarter call, Palantir’s management provided guidance about their expectations for Q2 and the remainder of the year.

They anticipate revenues reaching $936 million and adjusted revenues of $403 million at the midpoint of their guidance. Achieving these figures would mean growth of 38% and 59% year-over-year, respectively.

Looking back at the past three years, the chart depicting Palantir’s stock price trends reveals some interesting information. I even noted revenue reports with purple circles labeled “E.”

Since the wave of AI innovation began in early 2023, Palantir’s stock has generally seen upward movements after each quarterly report—except for one notable instance earlier this year.

After a remarkable Q1 report in May, the stock lost 12%, which seemed surprising. Yet, the decline didn’t stem from revenue missteps or what management discussed in their calls.

Instead, the surge in Palantir’s stock has led to increased scrutiny on the operational metrics. Investors have high expectations, even in light of impressive software performance and substantial growth. This raises the question: Is simply delivering “good” results enough anymore?

Despite the previous downturn, Palantir’s stock has rebounded dramatically and is currently at an all-time high.

The included chart outlines the valuations of Palantir alongside other comparable companies. With the expansion of ratings over the long term, Palantir’s valuation has significantly outpaced that of its peers in enterprise software. Notably, the 127 price-to-sales (P/S) ratio is much higher than many companies during prior market peaks.

While I am optimistic about Palantir’s long-term prospects, it does feel like the valuation has been stretched a bit too far. Given the rising expectations, investing in such a momentum-driven stock at inflated prices seems a bit imprudent.

Even if the company outperforms its guidance, it wouldn’t be shocking to see a pullback post-Q2 report. On the flip side, if Palantir does miss its targets, the stock could face considerable downward pressure.

For my part, I feel it’s wise to hold off on investing until after Palantir reveals its second-quarter results. This way, investors can better assess the growth in revenue, operating profit margins, and other crucial insights that management may provide during the earnings call.

Keep these considerations in mind if you’re thinking about buying into Palantir Technologies.