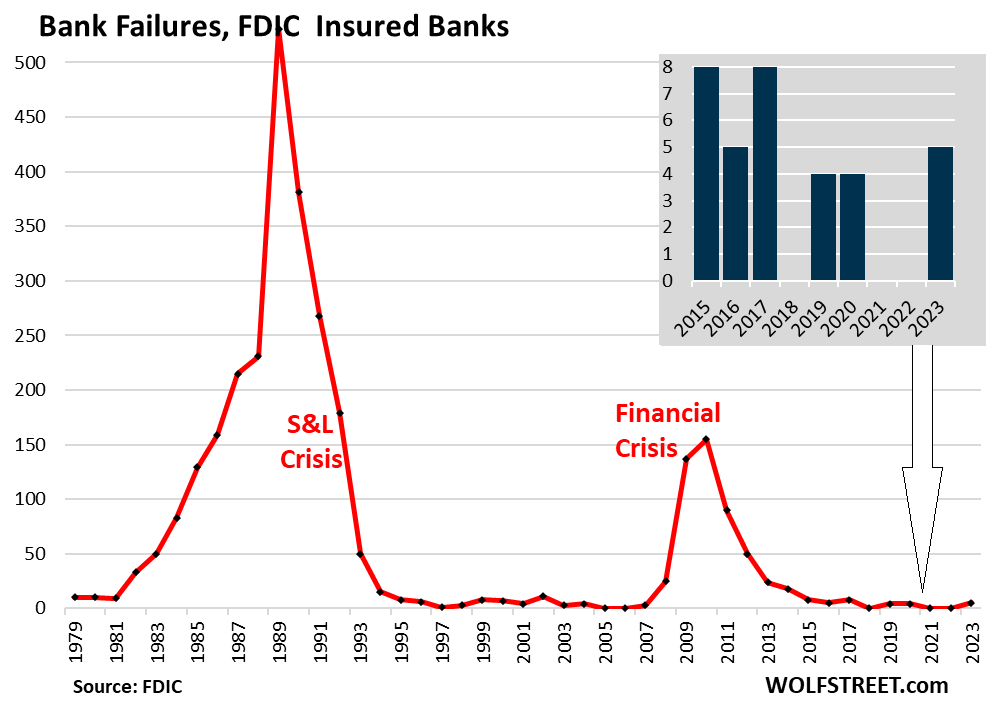

Several banks will fail in 2024. Five banks will fail in 2023. In 1989, more than 500 banks failed. Since 1936, there have been only five years without a bank failure.

Written by Wolf Richter of Wolf Street.

The plunge in long-term interest rates (now partially reversed) inspired by the rate cut mania at the end of the fourth quarter had a positive impact on commercial banks’ balance sheets, according to the FDIC’s quarterly bank data released Thursday.

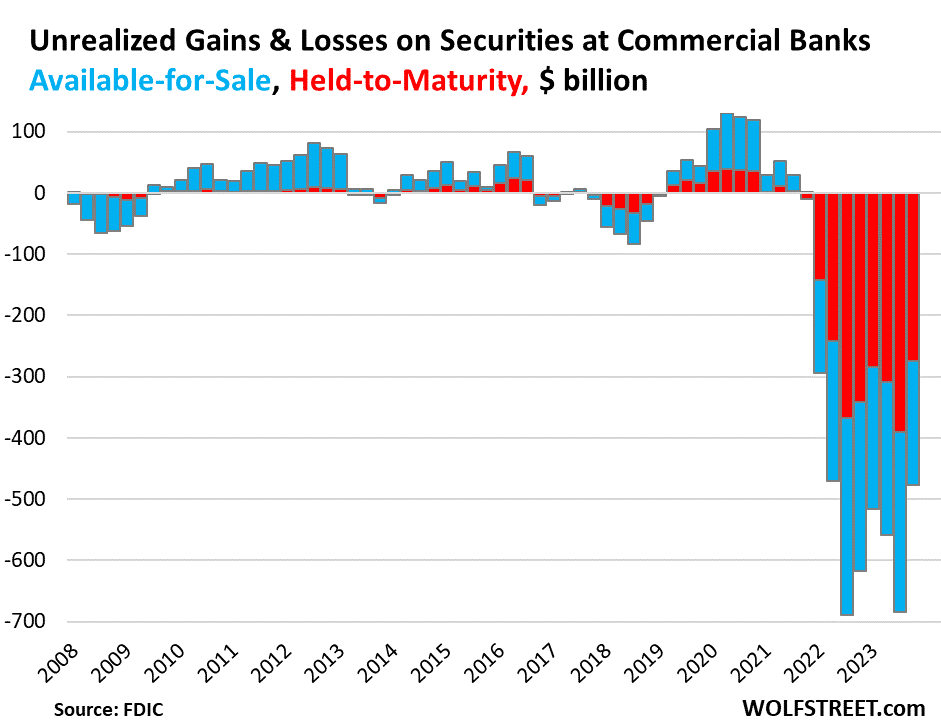

“Unrealized losses” on securities in the fourth quarter of 2023 decreased by $206 billion (or 30%) from the previous quarter, resulting in cumulative losses of $478 billion and $5.43 trillion in securities held by these banks. This corresponded to 8.8% of the total. Securities are primarily Treasury bills and government-guaranteed MBS.

These unrealized losses were spread over two accounting methods:

- HTM: Unrealized losses on $2.5 trillion of held-to-maturity (HTM) securities decreased by $116 billion from the previous quarter, resulting in cumulative losses of $274 billion (total shown in red in the chart below).

- AFS: Unrealized losses on available-for-sale securities (AFS) of $2.93 trillion decreased by $90 billion from the previous quarter to $204 billion (blue).

Those paper losses began to pile up in 2022, when the Fed began tightening monetary policy and bond yields rose. Long-term securities are particularly affected by rising yields. Higher yields mean lower prices.

As such, as yields rise in 2022, the market prices of these securities will fall, with record highs given the large amount of long-term securities that banks piled onto their balance sheets during the pandemic, when they were at near 0%. Unrealized losses piled up.

At the time, the Fed was printing trillions of dollars, some of which ended up on deposit in the banking system, and banks, unhappy with the near 0% yield on Treasury bills, were pouring this cash into longer-dated securities to yield higher yields. I got it. It was above 0%.

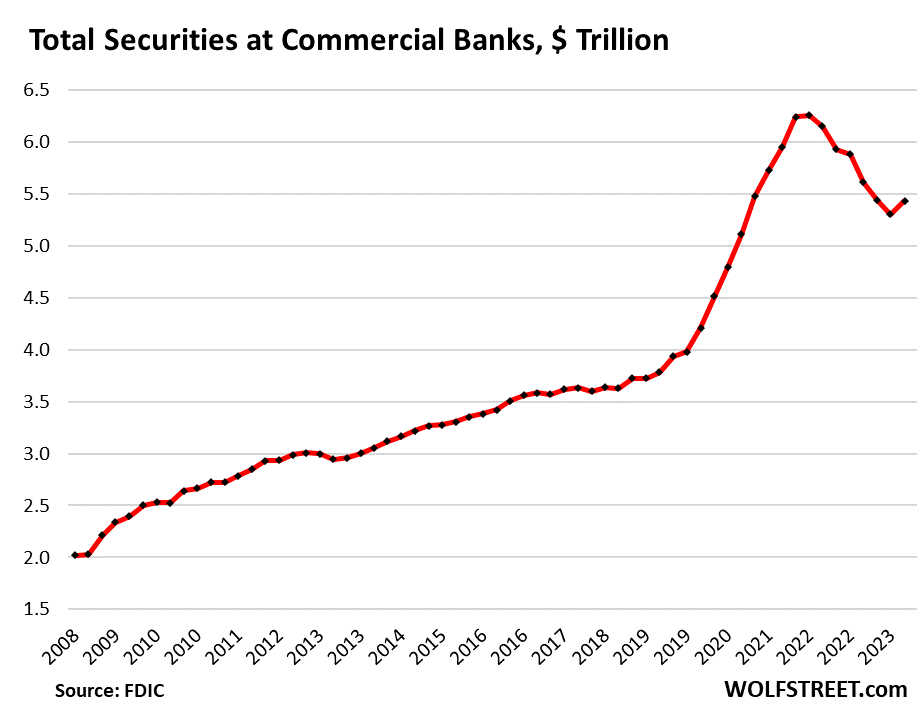

Total securities on a bank’s balance sheet.

During the money-printing era of the pandemic, the total amount of securities held by banks surged by $2.5 trillion, or 57%, to peak at $6.2 trillion in the first quarter of 2022.

Including the increase in the fourth quarter, that amount decreased to $5.43 trillion by the end of 2023. And the long-term securities in this pile have lost a lot of market value. There are several factors contributing to this decline, including:

- The portion of a failed bank’s securities that the FDIC sold to non-banks is no longer part of it.

- Banks value AFS securities at market value.

- Some securities have reached maturity

- Banks may have sold some securities.

The $5.43 trillion in securities includes securities valued at market value and securities valued at purchase price.

Banks are not required to mark these securities to market value, but can treat them at purchase price. The difference between market value and purchase price is an “unrealized gain or loss” that banks must disclose in their quarterly financial reports.

In theory, “unrealized losses” on securities held by banks are not a problem. At maturity, the bank is always paid the face value, and the unrealized loss decreases as the security approaches maturity and reaches zero at maturity. Maturity date.

But with the disclosure of these unrealized losses, uninsured depositors realized what was going on and began withdrawing their funds from Silicon Valley Bank, Signature Bank, and First Republic based on two basic principles of investing: .

- Those who panic first are the ones who panic most often.

- After me is the flood.

However, banks are unable to sell these securities to raise the cash needed to finance this outflow, as unrealized losses become realized losses, and banks are unable to obtain sufficient cash. Unable to do so, the company was in debt.

Loans and securities with remaining terms:

- Over 15 years: 14.5% of total assets, almost stable in 2023.

- 5-15 years: 14.2% of total assets, the lowest since Q3 2020.

- 3-5 years: 8.4% of total assets, the lowest since Q3 2022.

bank failure.

According to FDIC data dating back to 1936, there was only a five-year period in which an FDIC-insured bank did not fail. During the two years of free money due to the pandemic, no banks failed in 2021 and 2022. No banks failed in 2018. In 2006 and 2005, no banks failed. That’s it.

During the remaining 88 years, several banks failed. In 1989, during the peak of the S&L crisis and the post-oil crisis period, 531 banks failed and people actually went to jail for it. In the 2010 financial crisis, 155 banks failed. But by then, the bank was much bigger than he was in 1989. Then, the unthinkable happened and none of them went to jail. Instead, bankers at bailed-out banks earned record bonuses.

In 2023, six banks failed: Silicon Valley Bank, Signature Bank, and First Republic Bank, and two very small banks in Iowa and Kansas were taken over by the FDIC. Silver Gate Bank agreed to self-liquidation after being grilled by regulators, but the FDIC did not classify the bank as a “failed bank” because it had enough assets to cover its deposits without FDIC intervention. Not considered. In other words, there were officially five “failed banks” and one bank in self-liquidation.

Several banks will fail in 2024. We pretty much know that. I don’t know how many people there are. If eight banks go bankrupt, it will be at the same level as in 2015 and 2017.

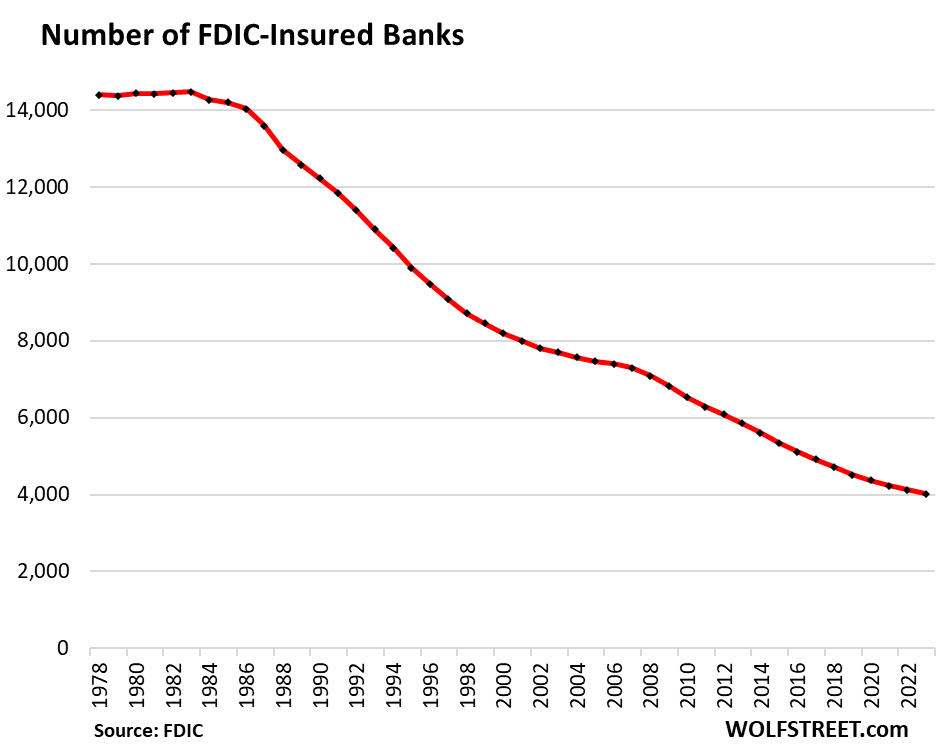

Commercial banks are disappearing one after another. In 2023, 100 banks will disappear due to mergers. Six banks went bankrupt due to bank failures and self-liquidation. However, six new banks were established. As of the end of 2023, the number of commercial banks has declined from more than 14,000 in the 1980s to 4,026.

Enjoy reading and supporting Wolf Street? You can donate. I appreciate it very much. Click on the beer and iced tea mugs to see how.

Would you like to receive email notifications when new articles are published on WOLFSTREET? Sign up here.

![]()