Market Update: S&P 500 Up 17% Amid Mixed Sentiments

This year, the S&P 500 has climbed 17%, reaching new all-time highs, which is pretty remarkable, especially since the market took a significant hit earlier this spring. Since its lows in April, it’s bounced back by roughly 37%.

While there’s a lot of excitement on Wall Street, some experts advise caution. Savita Subramanian from Bank of America has pointed out some bearish signals that investors should note. She mentions that their bear market indicators are flashing warnings, with 60% of them currently triggered. This is just shy of the historical average of 70% for pre-peak indications. However, she also acknowledges that comparing today’s market to the past can be tricky. The current S&P is, after all, considered higher quality and less leveraged.

I guess what really stands out is how Bank of America’s analysts are being quite selective, focusing on stocks that they think have room to grow. They’ve highlighted two picks worth exploring further, so let’s take a closer look.

Doximity: A Closer Examination

First up is Doximity, which serves as a networking platform for professionals in the medical field. Primarily aimed at physicians and direct care providers, the platform allows users to connect, keep up with medical news, and even conduct secure video appointments with patients. Doximity has designed its service to align with the mobile nature of modern healthcare, facilitating easier communication.

Promoted as the largest online network for U.S. clinicians, Doximity claims that about 80% of U.S. physicians and half of nurse practitioners or physician assistants are verified members. By harnessing a mobile app, it simplifies collaboration and sharing of essential medical developments.

The rising demand for medical services over the last ten years has propelled healthcare providers to adapt quickly, incorporating telemedicine into their practices. The Doximity app streamlines patient interactions, allowing providers to manage calls while tackling other tasks, thus enhancing efficiency.

To bolster its tech capabilities, Doximity recently acquired Pathway Medical for $36 million, a Canadian firm specializing in medical AI. This will integrate valuable physician-oriented AI resources into Doximity’s offerings.

Financially, Doximity reported $145.9 million in revenue for Q1 of FY26, showing a year-over-year increase of 15%. This figure surpassed estimates by over $6 million. The company also saw an increase in its non-GAAP EPS, which rose to 36 cents this quarter from 28 cents a year ago, exceeding expectations as well. They noted a significant 52% increase in free cash flow, climbing to $60.1 million.

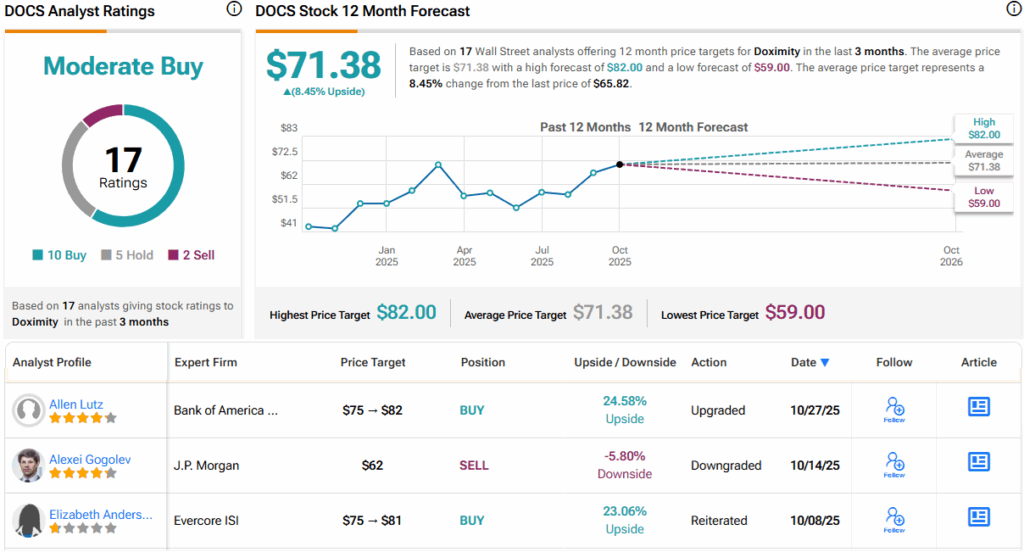

Bank of America’s analyst, Allen Lutz, is optimistic about Doximity’s positioning. He views current regulatory shifts as beneficial for the firm, noting how drug manufacturers are reallocating their promotional budgets more towards healthcare providers, benefiting platforms like Doximity. Following these observations, Lutz maintains a “buy” rating on Doximity, with a price target forecasting a 24.5% increase within a year.

Wayfair: Insights and Trends

Next is Wayfair, which specializes in online retail for home goods, particularly in furniture. Since its founding in 2002, Wayfair has grown to include around 21 million active customers, with an extensive inventory of over 30 million products. Headquartered in Boston, it’s become one of the largest retailers in the home goods sector.

Wayfair operates several brands, allowing it to cater to diverse customer needs, offering everything from home improvement items to pet supplies. The company sells predominantly online but also has physical stores in select states. Its ability to manage an expansive distribution network contributes to its operational efficiency.

In its recent quarterly results for Q3 2025, Wayfair reported a slight drop in active customers but noted a 6.1% increase in revenue per customer, which is promising. Their sales reached $3.1 billion during the quarter, up nearly 7% year-over-year, surpassing expectations significantly. Their earnings also saw a considerable bump from last year.

Michael McGovern from Bank of America holds a favorable outlook for Wayfair, suggesting that the company is well-positioned for future growth as the home goods market continues to evolve. McGovern believes that as online shopping increases, Wayfair’s extensive distribution network could yield more market share.

Analysts generally agree, rating Wayfair as a Moderate Buy based on several recent reviews, with identified growth potential of around 10% over the next year. Its stock currently sits at $102.40, with a price target averaging at $112.22, indicating optimism about its trajectory.