Market Analysts Reassess Valuations Amidst Stock Surge

(Bloomberg) – Recently, the stock’s value has shot up dramatically, causing market skeptics to voice their concerns, suggesting that now might not be the best time to invest.

Despite appearing “overpriced,” relying on traditional metrics to guide market timing has often proven unreliable, as past strategies haven’t always held up well.

Interestingly, there’s a growing number of Wall Street analysts who argue that it may be time to rethink historical notions around prices and returns, particularly with average multiples increasing consistently over the years.

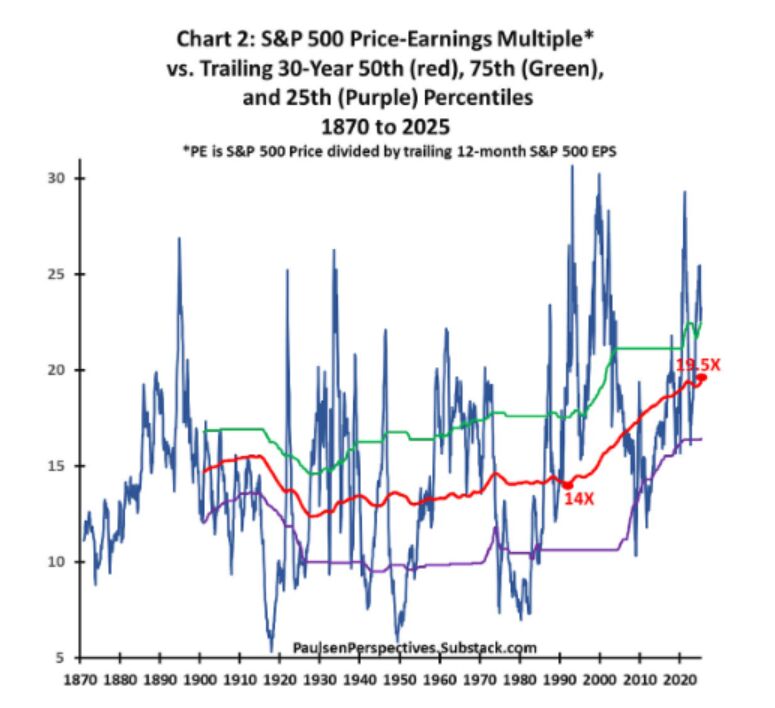

A recent study by veteran strategist Jim Paulsen indicates that average rating ranges have significantly increased over the past century, pointing out that comparing historical data may not be the best approach anymore.

For instance, Paulsen’s analysis reveals that the average price-to-revenue ratio for the S&P 500 was about 14 during the early 1990s, whereas it now hovers around 19.5. Before this surge, the ratio remained fairly stable between 13.5 and 15.5 from the 1900s until the mid-1990s.

“There’s something peculiar about past ratings,” Paulsen mentioned, highlighting a noticeable upward trend in the ratings over time.

This increase in stock ratings over the last 30 years could potentially counter arguments suggesting that the current excitement around artificial intelligence might face a fate similar to the late 1990s internet bubble.

According to Paulsen, this shift prompts a couple of key questions. First, how can investors effectively determine ever-changing valuation targets?

He offers several explanations for this trend upward, suggesting that more costly stock markets may simply reflect a new norm. For instance, the frequency of recessions in the U.S. has decreased significantly, from about 42% before World War II to roughly 10% in the last three decades. The U.S. economy has transitioned from being industrial-based to one that’s primarily technology and services-oriented, resulting in a market that’s increasingly favoring growth stocks that command higher valuations.

Add to that the improvements in stock market liquidity, thanks to the rise of electronic trading and greater participation from individual and international investors. Paulsen refers to the ongoing increase in profit productivity—the actual profit generated per worker—as a factor contributing to a persistent upward valuation bias. Furthermore, the pace of innovation has notably accelerated throughout history.

Paulsen isn’t alone in suggesting that today’s market could justify higher valuation levels. A strategist from Bank of America recently echoed this sentiment, noting that specific features of the current S&P 500—including lower financial leverage, reduced revenue volatility, and improved efficiency—support this rising trend.

“The index has transformed significantly since the 1980s, 1990s, and 2000s,” Savita Subramanian, head of equity and quantitative strategy at Bofa, stated in a note to clients. “Perhaps we should view it through a new lens, rather than hoping for a return to historical averages.”

Jonathan Golub, Chief Equity Strategist at Seaport Research Partners, added that the low multiples experienced in the 1970s and 1980s were largely due to high-interest rates affecting capital costs and the operational viability of businesses. While he doesn’t foresee that kind of risk now, he cautioned that if borrowing costs were to increase dramatically again, the multiples might revert to those lower levels seen in previous decades.

“We don’t believe we’re in a situation where multiples will continue to rise indefinitely. Instead, it feels more like we’ve adjusted to a new, higher level,” Golub concluded.