Mitch Rochell, managing director at Madison Ventures Plus, argues that if Varney & Co. has a supply-side problem, anything that drives demand for housing is unwise.

Nearly 1 in 10 American homeowners say they have withdrawn money from their retirement savings to cover the down payment and closing costs associated with a home purchase.

A recent study by Bankrate found that 9% of homeowners withdraw from a 401(k) or other retirement account for a purchase, and younger generations are most likely to do so.

The Washington Post releases a new report detailing how the nation’s top home builders are choosing to build smaller homes than ever before in light of the current housing crisis. did. (Reuters photo)

16% of Gen Z respondents (ages 18-27) and 12% of Millennials (ages 28-43) said they withdraw money from their retirement savings for a down payment, compared to 7% of respondents were aged 44-59. 8% of baby boomers (60-78 years old).

Fed says it is still planning three rate cuts and holds interest rates unchanged

But is it a wise economic move?

“401(k)s and other retirement programs are the most powerful wealth-building tools out there,” said David Ragland, CEO of IRC Wealth and certified financial planner. , does not recommend withdrawing from these funds to purchase a home.

He cited two main reasons for not being able to withdraw funds from retirement funds.

First, younger generations will be hurt far more than older generations because savers will lose out on the growth they would have had if they had kept their money in the fund for a long time. Become.

A “for rent” sign outside an apartment building in the East Village neighborhood of New York City on Tuesday, July 12, 2022. (Gabby Jones/Bloomberg via Getty Images/Getty Images)

The second biggest drawback is that the government takes most of the money you withdraw from your retirement account.

Ragland explained that after deducting federal and state taxes and a 10% withdrawal penalty, you’ll end up paying 40% on every withdrawal.

Rent or buy? Things to consider when deciding between a house or an apartment

To illustrate the impact, he presented a hypothetical scenario of a 30-year-old man who needs a $20,000 down payment and wants to take it out of his retirement savings. Because of the penalties, in this scenario the individual would actually have to withdraw his $33,000 from his retirement fund to cover the hit from the government.

But if that 30-year-old left $33,000 in a 401(k) without withdrawing it, by the time he or she was 85, that amount would have grown to $1.2 million (a typical 7 ). % Profit rate.

“Instead of making a $30,000 decision, you’re making a $1.2 million decision,” Ragland said. “That’s why you don’t do it.”

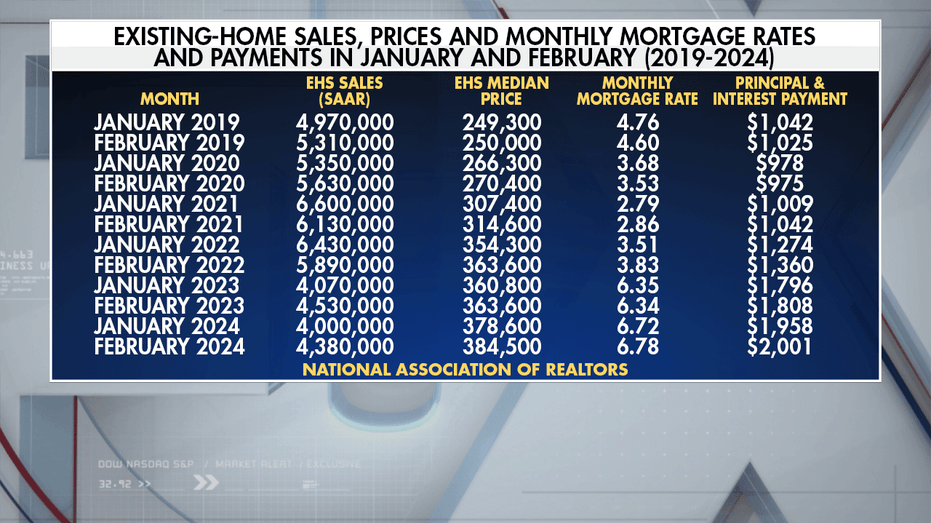

Data table showing existing home sales, prices, mortgage rates, and mortgage payments for January and February from 2019 to 2024. (Fox News/Fox News)

But for people who have retirement savings but no other way to come up with a down payment, Ragland offered an alternative option.

CLICK HERE TO GET FOX BUSINESS ON THE GO

He noted that people with 401(k)s can take out loans of up to $50,000 against these funds. This allows people to keep their funds in a retirement account while receiving the down payment they need while avoiding taxes and penalties.