At Credible Operations, Inc. (NMLS No. 1681276, hereafter referred to as “Credible”), our goal is to give you the tools and confidence you need to improve your financial situation. While we promote products from partner financial institutions from whom we receive compensation for our services, all opinions are our own.

We provide weekly updates on the latest trends in personal loan interest rates from the Credible marketplace. (iStock)

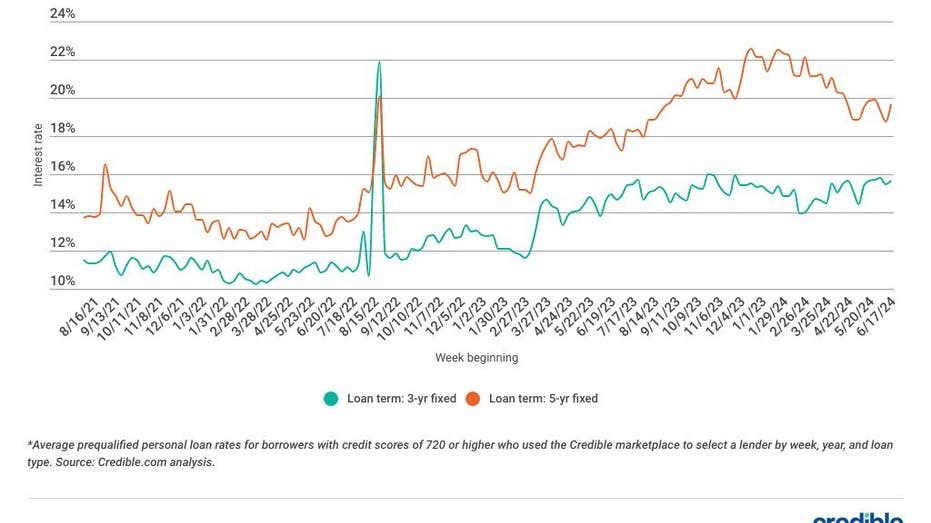

High credit rating borrowers Personal Loans In the past seven days, you’ve been pre-qualified for a lower interest rate for a three-year loan and a higher interest rate for a five-year loan compared to a fixed-rate loan in the seven days prior to that.

For borrowers with a credit score of 720 or higher who used the Credible marketplace to select a lender between June 20 and June 26:

- The average interest rate on a three-year fixed rate loan is 15.55%, down from 15.63% seven days ago and up from 15.00% a year ago.

- The average interest rate for a five-year fixed-rate loan was 19.99%, up from 18.65% last week and 17.93% a year ago.

Personal loans have become a popular way to consolidate debt and pay off credit card debt and other loans, and they can also be used to cover unexpected emergency expenses like medical bills or major purchases. Funding home improvement projects.

Average interest rate for personal loans

Over the past seven days, the average interest rate on personal loans has decreased for three-year loans and increased for five-year loans. Rates on three-year loans have decreased by 0.08 percentage points, while rates on five-year loans have increased by 1.34 percentage points. Interest rates on three- and five-year terms are higher than the same period last year, increasing by 0.55 percentage points for three-year loans and 2.06 percentage points for five-year loans.

Still, borrowers can enjoy interest savings with a three- or five-year personal loan, as both loan terms offer lower interest rates on average than higher-cost borrowing options like credit cards.

But whether a personal loan is right for you depends on a variety of factors, including what interest rate you can borrow, which is primarily based on your credit score. Comparing multiple lenders and their interest rates can help ensure you get the best personal loan for your needs.

Before applying for a personal loan, consider using a personal loan marketplace like Credible. Comparison Shopping.

Weekly Personal Loan Interest Rate Trends

Below are the latest trends in personal loan interest rates from the Credible marketplace, updated weekly.

The chart above shows the average pre-approval rate for borrowers with credit scores of 720 or higher who used the Credible marketplace to select a lender.

For May 2024:

- Interest rates on three-year personal loans averaged 22.35%, down from 22.65% in April.

- Interest rates on five-year personal loans averaged 24.52%, down from 24.53% in April.

Personal loan interest rates vary widely depending on your credit score and the length of the loan, so if you’re curious to know what personal loan interest rates you might qualify for, you can use online tools like Credible to compare options from different private lenders.

All lenders on the Credible marketplace offer fixed-rate loans at competitive rates. Because lenders use different methods to evaluate borrowers, we encourage you to request personal loan interest rates from multiple lenders so you can compare your options.

Current personal loan rates by credit score

Here are the average pre-approved interest rates selected by borrowers in May:

- 13.42% for borrowers with a credit score of 780 or above who choose a three-year loan

- 32.07% for borrowers with a credit score below 600 who choose a 5-year loan

Interest rates vary depending on factors such as your credit score, the type of personal loan you want, and the length of time you want to repay the loan.

As the chart above shows, a higher credit score can mean lower interest rates, while loans with fixed rates and longer repayment terms tend to come with higher interest rates.

Where are interest rates headed?

A lot has happened in the world of interest rates this week.

The Bureau of Labor Statistics (BLS) reported on Wednesday that inflation slowed in May, raising expectations of multiple interest rate cuts in 2024. Later that day, the Fed June Meetinghas signaled one rate cut by the end of the year while keeping rates on hold, and now expects one 25 basis point (0.25 percentage point) rate cut this year and a 100 basis point (1 percentage point) rate cut in 2025.

Currently, it is fluctuating between 5.25% and 5.50%. Federal Funds Rate It is the highest since 2001. Inflation is strong. Low unemployment rate A week ago, a rate cut seemed unlikely, but the news could come as a relief to borrowers with high interest rates or considering taking out a loan. Demand for personal loans debt levels and Delinquency rate has also risen, which could indicate that even if interest rates fall, more consumers may struggle to get approved for loans at low rates or may not be approved in the first place.

How to lower interest rates

Many factors influence the interest rate you’ll be offered by a personal loan lender. But there are steps you can take to improve your chances of getting a lower interest rate. Here are some tactics to try:

Increase your credit score

Generally, people with higher credit scores qualify for lower interest rates. Improve your credit score Over time this will look like this:

- Pay your bills on time: Payment history is the most important factor in your credit score, so pay all your bills on time.

- Check your credit report: Look at your credit report to make sure there are no errors, and if you find any, dispute them with the credit bureau.

- Lower your credit utilization ratio: Paying off your credit card debt can help improve this important credit score factor.

- Do not open any new credit accounts. Only apply for and open credit accounts you truly need. Too many hard queries on your credit report in a short period of time can lower your credit score.

Choose a shorter loan term

Repayment terms for personal loans can vary from one year to several years. Generally, the shorter the repayment term, the lower the interest rate because the lender’s funds are at risk for a shorter period of time.

If your financial situation allows, you may be able to get a lower interest rate by applying for a shorter term. Keep in mind that a shorter term doesn’t just benefit the lender; a shorter repayment term means you’ll pay less interest over the life of the loan.

Provide a guarantor

If you have student loans, you may be familiar with the concept of a cosigner. If your credit score isn’t high enough to qualify for the highest interest rates on a personal loan, finding a cosigner with good credit may help you secure a lower interest rate.

Remember, if you default on your loan repayments, the cosigner will be responsible for the repayments. Also, cosigning a loan can affect the cosigner’s credit score.

Compare interest rates from different lenders

Before applying for a personal loan, we recommend comparing offers from several lenders to find the lowest interest rate. Online lenders usually offer the most competitive interest rates and allow you to pay off your loan more quickly than brick-and-mortar lenders.

But don’t worry, comparing rates and terms doesn’t have to be a time-consuming process.

Credible makes it easy: just enter the amount you want to borrow, compare multiple lenders, and choose the one that’s best for you.

About Credible

Credible is a multi-lender marketplace dedicated to helping consumers find the best financial products for their circumstances. Credible is integrated with major lenders and credit bureaus so consumers can quickly compare accurate, personalized loan options without risking their personal information or impacting their credit score. The Credible marketplace delivers an unparalleled customer experience, as reflected by the following: Over 6,500 positive reviews on Trustpilot TrustScore: 4.7/5