Ends unchecked power of CFPB

The Consumer Financial Protection Bureau (CFPB) has become one of Washington's most powerful and least responsible agencies. Created under Dodd Frank in 2010, it was Elizabeth Warren's pet project, Progressive Financial Watchdog It is designed to operate out of reach of voters and elected officials. Unlike most agencies, the CFPB is not funded by Congress, but instead subtracts money directly from the Federal Reserve to protect it from normal budget oversight. For many years it was led by a single director who could not even be fired by the president. This is a blatantly unconstitutional structure that the Supreme Court overthrew in 2020.

For over 10 years, Conservatives pushed to suppress or dismantle the CFPBrecognizes it as a illegitimate bureaucracy with too much power and little accountability. Now, once President Donald Trump takes office, the fight has reached a new stage. Trump fired Rohit Chopra as CFPB director and nominated Jonathan McKernan as an alternative, but McKernan is still waiting for confirmation from the Senate. The contrast between the two couldn't be more dramatic. Chopra ran the agency through intimidation, with a decision made by press releases and enforcement action rather than explicitly regulated. McCernan, a financial lawyer and member of the FDIC board, is expected to bring about a more restrained pro-market approach, rolling back the worst excess of the institution and regaining the predictability of financial regulations .

Reversing Chopra's reign of regulatory chaos

Under Rohit Chopra, the CFPB was more than just a regulatory authority. The weaponized sector of progressive financial activism. Instead of issuing clear and predictable rules, Chopra is ruled by fear and uses media pressure, litigation and vague legal interpretations to force him to adhere to his ideological agenda. The financial sector didn't know what the rules were, but if they speculate that the CFPB is wrong, the CFPB might come after them.

One of Chopra's most controversial tactics was his habit of bypassing official rulemaking completely and presenting it instead. Changes to policy through press releases and enforcement actions. By circumventing legal procedures that write new regulations requiring public opinion and legal justification, it has made it impossible for banks, lenders and fintech companies to follow in advance. This resulted in a regulatory environment that was driven more by intimidation than the law.

He too Extended CFPB authority far beyond its original missionextensions such as UDAAP (unfair, deceptive, or abusive conduct and practice) and Ecoa (equal credit opportunity law) wipe out new rules for everything from overdraft fees to late credit card penalties. Justify justification. Chopra's CFPB also attempted to force non-bank financial companies into the new system of registration, giving supervision to institutions against businesses that Congress never intended to regulate.

On January 14, 2025, during an interview in Washington, DC, Rohit Chopra, director of the Consumer Financial Protection Bureau (CFPB) (Stefani Reynolds/Bloomberg via Getty Images)

The goal was more than just consumer protection. That was about Empower leftist bureaucrats To shape the financial system in their image, there is no need for legislation, not the need for legislation, just dictatts from high.

McCernan's Vision: A More Market-Friendly CFPB

Jonathan McCernan is not a Maga Fire brand, but it represents a serious change in his approach. Rather than pursuing the far-left social and economic agenda through financial regulations, he is expected to focus. Regulation clarity, enforcement fairness, and market efficiency– Everything that was so badly missing under Chopra.

One of the biggest changes is: Return to rules making for each execution. Rather than governing sudden enforcement actions, McCernan is expected to restore the process of writing clear, legally based regulations. This gives businesses a fair opportunity to understand and comply with the law rather than blinded by arbitrary CFPB oppression.

Another priority is to fix some of the CFPB's more dysfunctional regulations. Expect efforts to clean up the mess that Chop has left behind, such as reforming mortgage rules to make refinancing easier. Instead of using regulations to restructure the financial sector into an engine of progressive politics, McCernan is likely to focus To make the market better for both lenders and consumers.

Jonathan McCernan, co-chair of the Federal Deposit Insurance Corporation (FDIC) special committee, will speak at a House Financial Services Committee hearing held in Washington, D.C. on June 12, 2024.

Perhaps the most important change is a more rational approach to enforcement. At Chopra, minor compliance errors can lead to massive penalties, even if they are not harmful to consumers. McCernan is likely to do so Refocusing CFPB on chasing real fraud and predatory practices Rather than using enforcement as a political tool.

The broader change is philosophical. Previous CFPB leadership has been a form of protection, particularly under the Biden administration, restricting consumer financial choices is a form of protection, including preventing climate change and forcing the adoption of left and right sides. It was run on the assumption that financial regulations should be used to pursue broad social goals. Views on diversity, equity and inclusion. McCernan is expected to take the opposite view, Emphasise competition, choice and financial access Rather than forceful regulatory management and left-wing social engineering.

CFPB's Civil Penalty Fund: Slash Fund for Bureaucrats

One of the most obvious abuses of the CFPB's power is its civil penalty. A self-supporting slash fund that allows agents to bypass Congress completely. Instead of relying on budgets, CFPB funds by withdrawing fines from financial institutions and redistributing the money.

This will be created Clear conflict of interest. The more penalties the CFPB distributes, the more you control your money. Give agents evil incentives to escalate enforcement, whether they actually benefit consumers or not. The fund is supposed to compensate victims of financial misconduct. But in reality, it's used to Bankroll Progressive Financial Behaviorismperhaps directing money towards politically connected organizations, not individuals that are hurt.

If McCernan takes over, it will probably be like that. New pressures to increase transparency And it will strictly limit how these funds can be used. Some people in Congress may end the CFPB's ability to fully self-fund their own funds and force them to pass the normal budget, like other federal agencies.

Unsolved Battle: How far does Trump go?

McCernan's appointment shows a major change, but the bigger issue is that the Trump administration is Demolate CFPB's independent funding and executive bodies forever.

One possible move is to completely cut off CFPB funding. As agents rely on transfers of the Federal Reserve rather than Congressional budgets, some Trump allies like Russ push McCernan to reject those funds and effectively make cash I'm starving. It's going to happen Force Congress to explicitly fund or drain the CFPB.

CFPB budgets can be reduced without violating the Water Storage Management Act. (We say that Claim Do this because this law could be an unconstitutional infringement of Presidential authorities. ) Ironically, that's because of the very fundraising mechanism created by Elizabeth Warren to make the bureau independent. Congress has not properly funded the CFPB. Therefore, there is no problem with water storage.

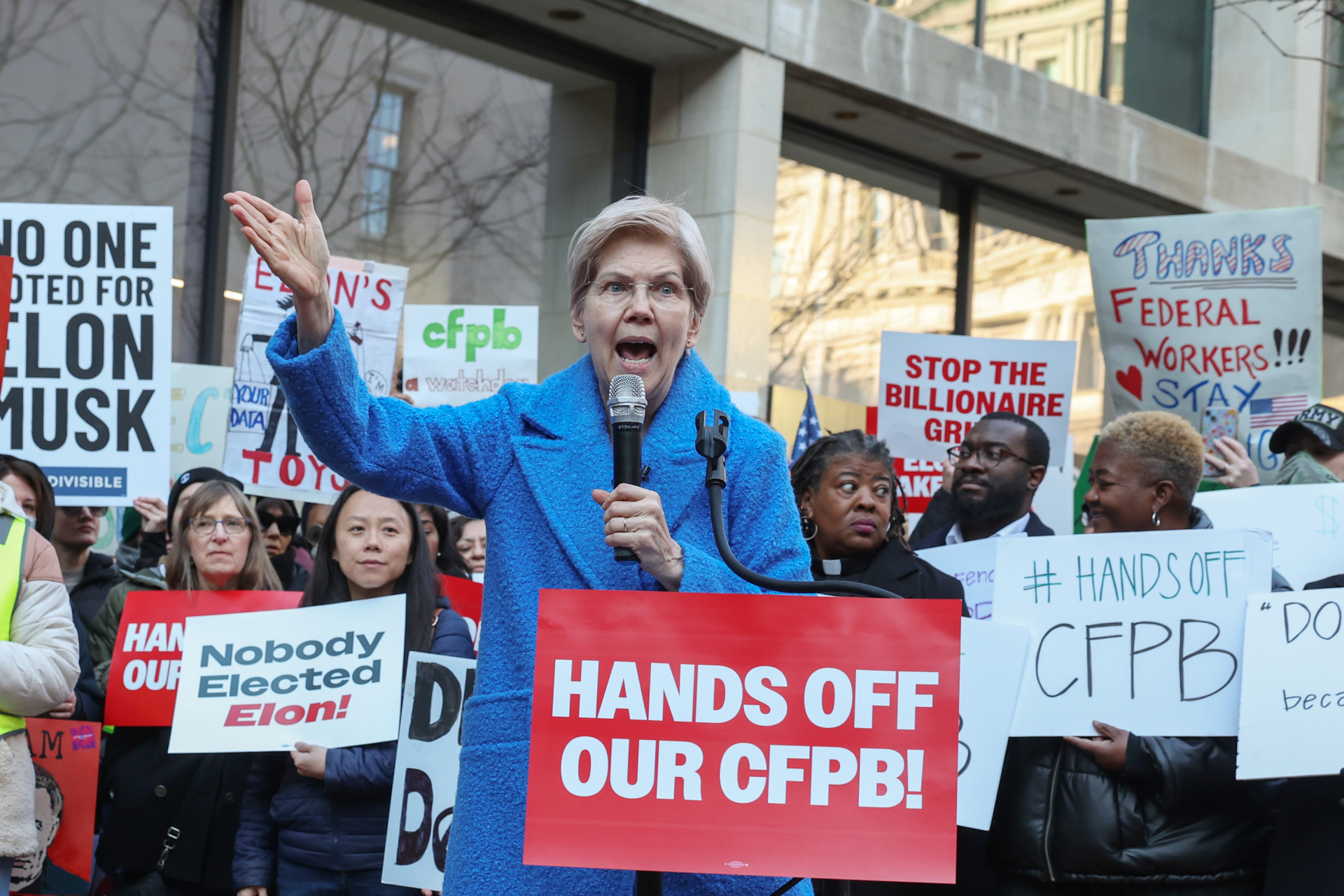

Sen. Elizabeth Warren (D-MA) will hold a rally in Washington, DC on February 10, 2025 to protest the closure of the Consumer Financial Protection Bureau (CFPB). (Jemal Countess/Getty Images on MoveOn)

Another question is how proactive the administration will roll back the agency's enforcement activities. Will McCernan close certain investigations? Can CFPB surveillance in a particular industry be completely eliminated?

And then there is the bureaucrats themselves. One of Trump's biggest challenges in his first semester was A steady administrative state That was against his agenda. If he wants to truly reform the CFPB, he will probably need it. Give out pink slips For most of the career staff.

The end of the era?

Elizabeth Warren designed the CFPB Immunity from conservative reformhowever, that unidentified power may finally be split. With Trump's return, the agency is under the original real threat of structural reform, and McCernan's confirmation battle will be something to watch. Senate Democrats are likely to delay and resist his nomination in order to keep the CFPB's progressive agenda intact.

But even if McCernan is confirmed, the real problem isn't just who will lead the agency.That's whether the current format of CFPB should exist at all. Legal challenges for fundraising are still pending that Republicans in the Supreme Court and Congress are looking for ways to limit their power, so agencies ultimately have a level of accountability that Warren never intended. You may be forced to do so.

What's certain is that CFPB's Unidentified Power Day is over. Next up is Trump, McCernan and the courts.