Executive Summary

-

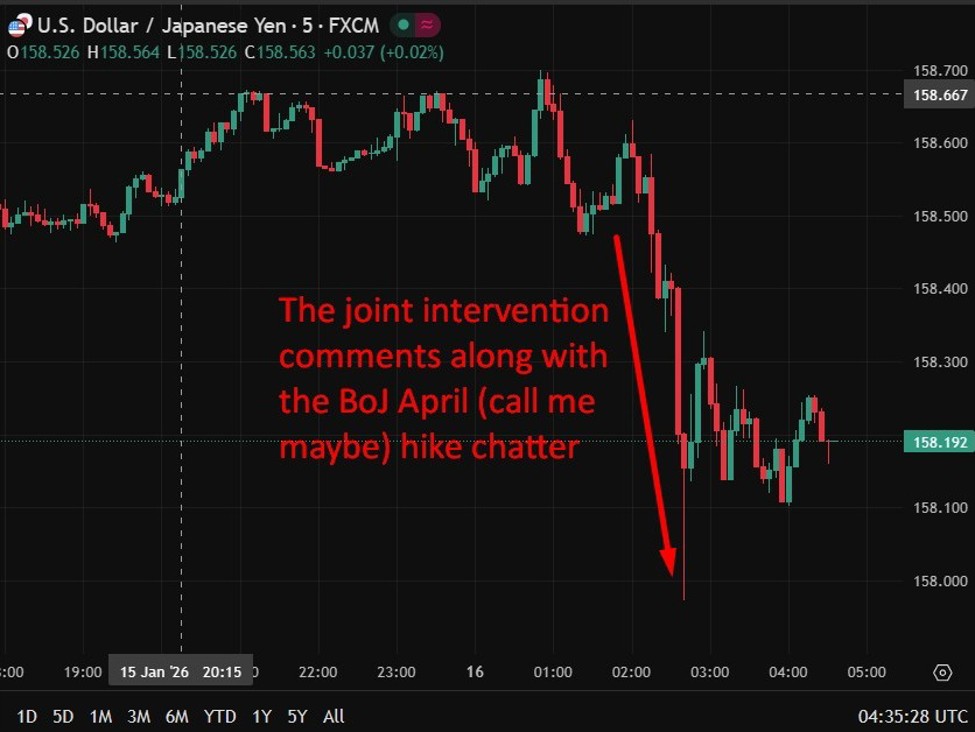

The yen saw gains after warnings of possible currency intervention and a report indicating that some members of the Bank of Japan are considering an early interest rate hike, potentially in April.

-

The New Zealand dollar experienced a slight increase, supported by strong manufacturing PMIs and a drop in food prices, which bode well for short-term growth and inflation expectations.

-

Concerns about U.S. trade policy have resurfaced, with the White House indicating that tariffs on AI chips are just a preliminary measure.

-

The European Central Bank suggests stability in interest rates but cautions that risks from U.S. monetary policy could impact global markets.

-

Geopolitical tensions have eased somewhat, as Iran has shown restraint. While oil prices rose, a decrease in safe-haven demand has impacted gold prices.

-

China has taken steps to limit high-frequency trading by moving servers out of exchange data centers, which will affect latency benefits.

The yen surged after Japan’s finance minister stated that foreign exchange intervention remains a viable option, emphasizing that measures, including collaborative actions, are still considered. Concerns about excessive currency fluctuations quickly affected market movements. The momentum increased with a Reuters report suggesting some Bank of Japan officials see a potential for raising rates sooner than anticipated, possibly in April, particularly if inflationary risks from the weaker yen persist. This highlights growing unease that a declining yen may lead to increased price passing through, complicating the Bank of Japan’s view that cost pressures would subside over time. The yen experienced a brief drop below 158.00 against the dollar before stabilizing.

Nonetheless, the yen has faced additional challenges this month due to political factors, as there’s speculation that Prime Minister Sanae Takaichi could gain more power for expansionary fiscal policies if she wins the election. This dynamic has led to ongoing structural pressures on the yen, making a substantial recovery difficult to achieve.

In the first half of the session, New Zealand’s economic data remained encouraging. The manufacturing PMI rose to 56.1 in December, its highest level since 2021, driven by growth in all sub-indices and new orders. The Bank of New Zealand pointed out potential upward risks to Q4 GDP and strong momentum into early 2026. Following this, the food price index showed a decrease, falling by 0.4% in November and 0.3% in December. While food prices are still up 4% year-on-year, these successive declines provide a positive signal for the Reserve Bank of New Zealand, contributing to modest gains for the New Zealand dollar.

Trade policy uncertainty has re-emerged in the United States after the administration imposed a 25% tariff on certain advanced AI chips earlier in the week. Officials stated that these measures are just the first phase, with further actions possible based on ongoing negotiations with foreign governments and companies.

In Europe, ECB Chief Economist Philip Lane reaffirmed that there would be no short-term discussions about interest rates if the current outlook remains unchanged. However, he cautioned that shocks from the U.S., including any deviation from the Federal Reserve’s mandates, could destabilize global financial conditions and prompt a reassessment in Europe.

On the geopolitical front, there were reports about a U.S. aircraft carrier moving toward the Middle East, although these were largely viewed as outdated. Iran’s deputy UN envoy stated that the country does not seek conflict but will respond strongly to any aggression. Crude oil prices opened slightly higher, but gold prices fell as reduced geopolitical tensions lowered demand for safe-haven assets.

Lastly, China has initiated measures to limit high-frequency trading by relocating server operations away from exchange data centers in Shanghai and Guangzhou, which will diminish latency advantages for both domestic and international trading firms.

Asia Pacific Stocks:

- Japan (Nikkei 225) -0.05%

- Hong Kong (Hang Seng) -0.27%

- Shanghai Composite -0.22%

- Australia (S&P/ASX 200) +0.42%

Have a great weekend! Looking forward to Monday’s influential China data on the agenda!