BlackRock and Bank of America have dropped their diversity, equity and inclusive policies. After the White House declared a woken war in Corporate America, it became the latest Wall Street giant to abolish the controversial initiative.

Regulatory submissions reviewed by the Post show that BlackRock, the world's largest asset manager, Larry Fink, is under $11.4 trillion control, with Brian Moynihan-led lenders in different minorities. X languages that promote group representation and participation.

The move follows a crackdown led by President Donald Trump on workplace day, which left Attorney General Pam Bondi in an executive order on January 21, asking her to stomp on her practice.

Bondi then vowed in a February 5 memo that her DOJ would “examine, eliminate, punish” such policies in the private sector.

In its latest annual report filed late Tuesday, BlackRock said its business “needs to attract the best people from around the world.”

“BlackRock is committed to creating an environment that supports top talent and promotes diverse perspectives to avoid group thinking,” the report added.

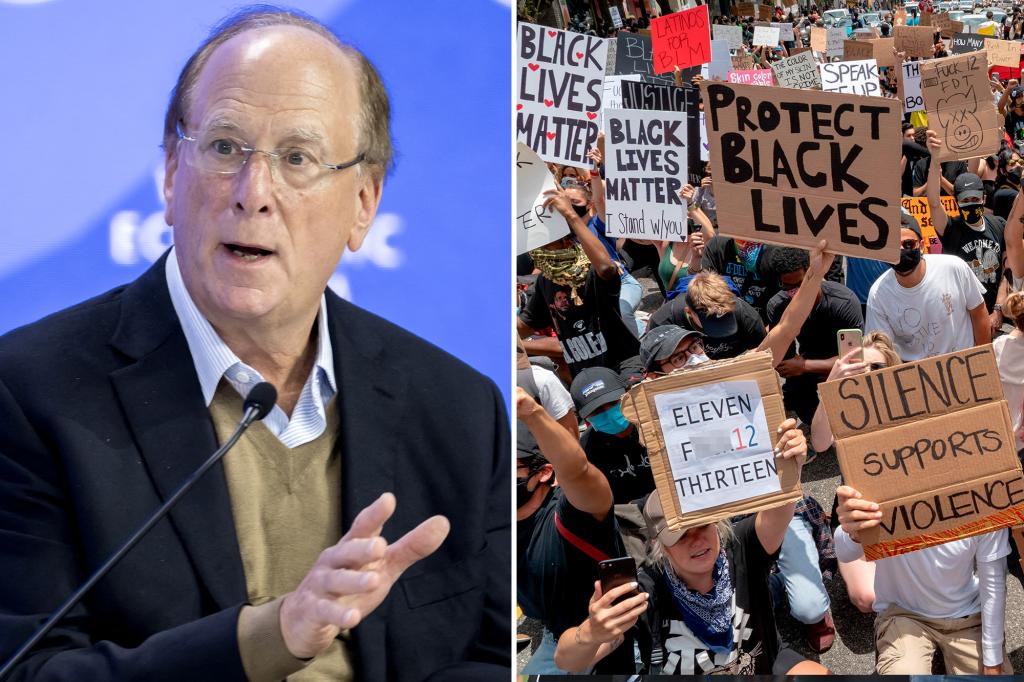

This represents the big climb of the Democratic CEO who joined the chorus of Wall Street executives who support Day in the aftermath of the 2020 George Floyd murder and the Black Live Matter movement.

In a letter to shareholders in 2021, Fink argued:

This post was contacted BlackRock for comment.

Bofa also supported the highly critical DEI policy in its annual report submitted Tuesday evening, and officially concluded the requirements for bankers' employment and interviews.

“We are cautious about the many ways we try to create an inclusive environment that everyone has.

The Charlotte-based company writes.

Bank of America officials confirmed that it is no longer a company policy.

“We will evaluate and coordinate the program in light of new laws, court decisions, and more recently executive orders from the new administration,” the spokesperson posted Wednesday.

“Our goal was to make opportunities available to all our clients, shareholders, teammates and the communities we serve.”

The day rollback by two giants in the US finances reflects what some of their rivals have been doing since Trump defeated Kamala Harris in a White House race on November 5th. It's there.

Wells Fargo, Citigroup and Morgan Stanley have also reduced DEI commitments, but Goldman Sachs recently cancelled the requirement that the company be publicly available only if they have two diverse board members.

JP Morgan CEO Jamie Dimon said the nation's biggest banks support its diversity policy despite slamming into the DEI initiative in leaked records of a city hall meeting with Chase employees. On Monday, they claim they are claiming that they are claiming on Monday.

Dimon told the audience he “didn't really believe in the prejudice training,” blowing up the company “we will spend money on some of this stupid shit.”

The Wall Street giant also rubbed much of the DEI language on investors in its recent annual report, further confirming mood changes at major American banks.

“Everyone in my industry wants diversity in the workplace that reflects the team and society as a whole, but everyone on Wall Street personally agrees that Day's doctrine has actually begun to go too far. People are afraid to speak up,” said Dan McCarthy, veteran Wall Street headhunter and CEO. Specialist Global Search Company, 1 search.

“My clients still employ diversity and they say they want to continue hiring diversity,” says McCarthy, the head of the young women, who has become a financial nonprofit.

“But some Dei policies have become toxic until they become discriminatory. It feels like we're beginning to see more common sense around it.”